Blog Post

Emerging market central banks and quantitative easing: high-risk advice

Central banks in emerging markets with weak currencies should not resort to unorthodox monetary tools such as quantitative easing as a response to the crisis triggered by COVID-19. Preferable alternatives include shifting public spending away from less pressing needs, moderately increasing public debt and falling back on official development assistance.

The idea that ‘credible’ emerging-market central banks (EMCBs) could embrace quantitative easing (QE) to tackle the consequences of the COVID-19 pandemic, as suggested by Benigno et al (2020), could cause more harm than good. Let us point out the main weaknesses and risks.

First: the different roles of core and peripheral currencies

The suggested approach largely disregards the different roles of ‘core’ and ‘peripheral’ currencies in international markets. While ‘core’ currencies, including the US dollar, the euro and, to lesser degree, the Japanese yen, British pound, Swiss franc and Chinese renminbi, play the role of international (global) money, in all its three functions, and are demanded by both domestic and foreign economic agents, ‘peripheral’ currencies are subject to only domestic demand. Furthermore, several EMCBs have been struggling for decades because of the limited credibility of their currencies, as a result of past currency and public debt crises, high inflation or hyperinflation episodes, shallowness and fragility of their financial sectors, and political instability. Consequently, their currencies are also challenged domestically by the currency substitution phenomenon.

The difference between core and peripheral currencies is fully evident in times of global financial turbulence, such as the emerging-market crises in 1990s, the global financial crisis (GFC) in 2008-2009, the collapse of oil and commodity prices in 2014-2016, and smaller episodes, such as those related to the expected QE tapering by the US Federal Reserve Board (Fed) in 2013. It can also be observed since February 2020 as result of the COVID-19 shock.

Global shocks, even if like the GFC they originate from advanced economies, trigger capital flight from emerging markets towards ‘safe’ havens in major currency areas. Investors replace holdings of emerging-market financial assets and denominated in emerging-market or peripheral currencies with highly-liquid assets denominated in core currencies. In addition, many EMCBs face greater degrees of currency substitution by residents in times of turmoil. That is, the global demand for core currencies increases while demand for peripheral currencies decreases. As a result, core central banks have more room for monetary easing, including the use of unconventional monetary policy measures, which sometimes they are forced to use to avoid deflationary pressures, while EMCBs have very little room for manoeuvre.

Sterilisation of capital outflows and lower demand for the domestic currency by increasing the money supply, regardless of which monetary policy instrument is employed to serve such a goal, would be risky if done by EMCBs, and might make matters worse. Unfortunately, the advice from Benigno et al (2020) reminds us of proposals from the so-called heterodox school in Latin America in the 1970s and 1980s, which advocated fiscal and monetary expansion to combating adverse external shocks. Too often, such policies led to macroeconomic catastrophe.

Second: the dangers of financing expansionary fiscal policy through monetary expansion

The Benigno et al. (2020) proposal goes far beyond an accommodative monetary policy and suggests expansionary fiscal policy financed by money emission. This is nothing new in the history of emerging-markets: many EMCBs financed government spending this way, usually with dire consequences. It took the last two decades to depart from this practice (indeed, this has not been successful everywhere) and to build, step-by-step, the actual independence of EMCBs in order to acquire greater degrees of confidence in these domestic currencies. Even then, confidence in peripheral currencies still remains far lower than in currencies of macroeconomically stable advanced economies, let alone core currencies. Whatever good intentions exist behind the Benigno et al (2020) proposal, it risks damaging what has been achieved in the area of EMCB independence, their credibility and the macroeconomic foundation of successful inflation targeting.

One may also ask whether printing money can really help in fighting the consequences of the COVID-19 pandemic. Higher inflation, the unavoidable consequence of large-scale monetary financing of government spending, will hit the poorest segments of the population and destabilise the entire economy. For sure, all governments – not only in emerging-market economies – must devote more resources to public health protection and income support for the most vulnerable, but this should be done by shifting public expenditure from less essential needs (for example, most emerging-market economies spend too much on their militaries) and moderately increasing public debt on commercial terms, rather than by printing money. In low-income countries, official development aid should play a more important role at this critical time.

Third: undermining hard-won historical gains

The suggested policies would also have negative political economy consequences by undermining decades of effort to build up the independence and credibility of EMCBs through the introduction of various institutional checks and balances, including in the public finance management sphere. While populist and myopic politicians might welcome the suspension or abandonment of such checks and balances, it would not be easy to reintroduce or activate them again.

Fourth: inflation is a greater risk than deflation

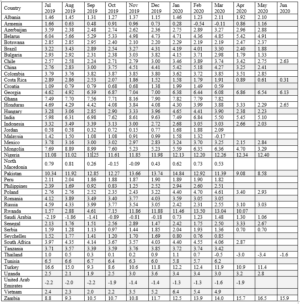

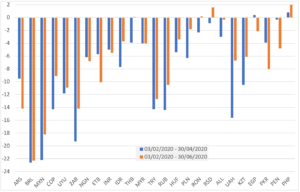

It is difficult to accept the diagnosis of Benigno et al (2020) that deflation risk is greater than inflation risk in emerging-market economies. Table 1 shows the opposite: many emerging markets continue to record either high one-digit or two-digit inflation and, in several countries, inflation has recently been increasing rather than decreasing. Only Thailand and the United Arab Emirates have recorded negative inflation. Currency depreciation experienced by several emerging markets as a result of the COVID-19 financial shock (Figure 1) might push inflation up rather than down.

Table 1: 12-month inflation in selected emerging-market economies, in %, July 2019 – June 2020

Source: IMF International Financial Statistics, accessed on 14 July 2020.

Figure 1: Changes in the exchange rate of emerging-market currencies (in US$ for a currency unit), in %, between 3 Feb 2020 and 30 June 2020

Source: Bloomberg.

Here we touch on an important question on the nature of the current crisis. Unlike during the emerging-market crises of the 1980s and 1990s and the GFC, the current crisis is a combination of demand-side and supply-side shock, resulting, at least in the first stage of fighting the pandemic, mainly from prohibition of certain types of activities, the movement of people, closed borders and disruption of supply chains. In such circumstances, private spending decreases and private savings increase, but these are forced savings, similarly to centrally planned economies where people could not spend their income on the goods and services they wanted to buy because they were not available.

In terms of monetary arithmetic, forced savings mean additional demand for money balances, which creates a kind of temporary buffer against the increased supply of money caused by monetary and fiscal expansion. The key questions are how big this buffer is, and how quickly it will disappear once lockdown is relaxed. At the moment, nobody knows the answers to these questions. One can only guess that in the case of core currencies, for which there is a greater external demand in times of crisis, this buffer is larger than for peripheral currencies, many of which experience a declining net demand as a result of capital outflow and currency substitution. This difference should suggest that EMCBs and emerging-market governments should be extremely careful in embracing discretionary monetary and fiscal stimulus.

Fifth: what is credible?

While Benigno et al (2020) addressed their proposal to credible EMCBs, they do not define explicitly which central banks are credible. Indirectly, one may guess that they have in mind “…countries with flexible exchange rate regimes and well-anchored inflation expectations.” However, one can rarely determine ex ante whether inflation expectations are really well-anchored, especially in times of strong external shocks associated with capital outflows and currency depreciation. Regarding flexible exchange rate regimes, the question is even more complicated. In such regimes the exchange rate serves as a shock absorber. In case of adverse shocks, this means currency depreciation. In ‘normal’ circumstances, a weaker currency can help boost exports and reduce imports, and sometimes also increase budgetary revenues, in the case of commodity exporters, but at the cost of reducing internal demand, thus having a contractionary effect, and increasing local-currency equivalents of both public and private foreign-currency denominated debt. Thus, it is a double-edged sword. Where there are administrative constraints justified by public health considerations and partly disrupted international trade links, a weaker currency might not help exporters.

Rather we would suggest that emerging-market economies with large international reserves or sovereign wealth funds, low public debt (below, say, 30% of GDP), low annual inflation (below 3-4%) for at least a decade, a relatively stable exchange rate for several years, and which have not experienced financial crises or high inflation in the last two decades, may embrace more expansionary fiscal and monetary policies when necessary. As most EMCBs have policy interest rates still above the zero level, sometimes well above this, they should use conventional monetary policy tools in the first instance.

Sixth: long-term risks

Benigno et al (2020) provided data on three-day cumulative change in selected countries’ ten-year government bond yields and the percent change in bilateral exchange rates versus the US dollar, following the announcement of the start of QE. This may suggest that QE is a risk-free instrument in EMCBs’ hands. However, financial market reaction to policy decisions is not always immediate. Quite often, the effects of such decisions cumulate over time and explode when there is an additional shock. One may use the analogy of walking on melting ice on a lake, where the first few steps seem safe but then the ice breaks suddenly. Thus, it is better to observe longer-term data trends before assessing the actual macroeconomic and financial fragility of EMs.

If we take the period between February and June 2020 (Figures 1 and 2), the negative shock looks powerful, especially in March and April. Thereafter, it subsided somewhat in emerging Asia[1], central and eastern Europe, and some oil-exporting countries. However, it remains serious in Latin America, Middle East and Africa, and the former Soviet Union.

[1] The Emerging Asia region has been relatively resilient to financial shocks, during both the GFC and the current crisis.

This is not the end of the story. The COVID-19 related crisis is only in its first stages and nobody knows how long it will last and what it will look like in the next months. This is an additional argument in favour of prudent macroeconomic policies and the avoidance of risky experiments.

References

Benigno, G., J. Hartley, A. García-Herrero, A. Rebucci and E. Ribakova (2020) ‘Credible emerging market central banks could embrace quantitative easing to fight COVID-19’, Bruegel Blog, 6 July, available at https://wordpress.bruegel.org/2020/07/credible-emerging-market-central-banks-could-embrace-quantitative-easing-to-fight-covid-19/

Dabrowski, M. (2016) ‘Core and periphery: different approaches to unconventional monetary policy’, Bruegel Blog, 24 May, available at http://bruegel.org/2016/05/core-and-periphery-different-approaches-to-unconventional-monetary-policy/

Dabrowski, M. and M. Dominguez-Jimenez (2020) ‘Is COVID-19 triggering a new emerging-market crisis?’ Bruegel Blog, 30 March, available at https://wordpress.bruegel.org/2020/03/is-covid-19-triggering-a-new-emerging-market-crisis/

Republishing and referencing

Bruegel considers itself a public good and takes no institutional standpoint. Anyone is free to republish and/or quote this post without prior consent. Please provide a full reference, clearly stating Bruegel and the relevant author as the source, and include a prominent hyperlink to the original post.