Blog Post

Juncker plan: the EIB in the driver’s seat

After weeks of negotiations with the European Commission and the Council of the EU, the European Parliament on 24 June adopted the text establishing the European Fund for Strategic Investment (EFSI), the instrument at the centre of Commission president Jean-Claude Juncker's investment plan. Now that the details of the plan are available we can assess more precisely how it will work and what its impact might be on European growth and employment.

What is EFSI for?

The plan tries to address the dramatic fall in investment affecting Europe since the beginning of the crisis. The yearly level of investment is currently around 10 percent (or almost €300 billion) below its long-term trend (excluding bubbles), as discussed in a previous Bruegel blog post. This fall in investment has been a significant drag on growth and employment for six years now, but it will also hold back Europe’s growth potential in the long-term. In that respect, the plan is a step in the right direction: since the beginning of his mandate, President Juncker has highlighted investment as one of his key priorities, and the investment plan was the new Commission’s first flagship project.

The Juncker plan, a second-best solution?

However, the optimal response to the fall in investment would have been a massive European public investment plan either through the European Investment Bank (as suggested for instance by my colleague Zsolt Darvas), through the member states (with, for instance, the help of an improved investment clause to exempt public investment from fiscal rules), through a re-oriented European Stability Mechanism, or through another institution created for the occasion, in order to take advantage of the historically low interest rates from which European governments have benefited since mid-2014.

The solution proposed by the Commission shows that a majority of member states had no appetite for such a massive public investment plan, and the Commission has brought together only a very small amount of money relative to the extent of the investment problem affecting Europe today. The funds devoted to the Commission’s flagship investment project will consist only of €8bn from a reshuffling of EU budgets from 2015 to 2020 (representing only half of the total €16bn pledged by the Commission to the EIB), and €5bn from the past profits of the EIB.

Given that the Commission has been heavily constrained by the limited funds allocated to the plan, its initial idea was to use the funds to offer guarantees to risk-averse private investors in order to finance high-risk/high-return investments. At the time, this seemed like a smart idea, and a possible second-best solution, as long as the guarantee was offered for investments that were not able to find financing, as we explained in another blog post published when the plan was revealed at the end of November 2014.

Is the Juncker plan really what the Commission claims it is?

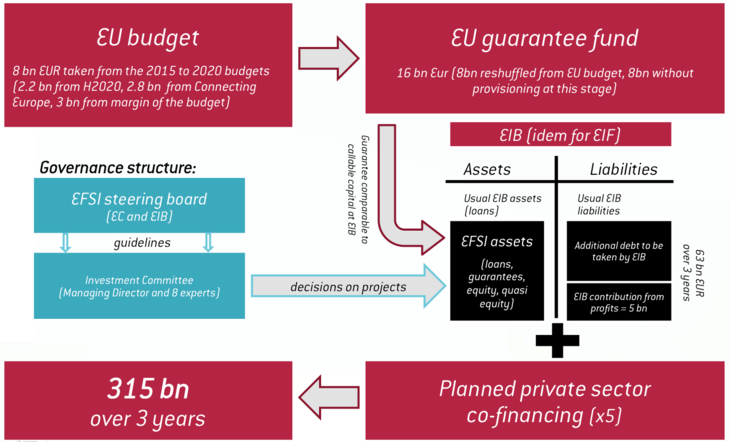

However, looking at the details of the plan approved last week by the European Parliament, there are now some good reasons to be sceptical and to think that the plan’s impact on growth and employment will be negligible. First, although EFSI is presented as a proper fund, it is important to understand that it will just be a label for some of the new EIB assets. This label will be awarded by the newly created “EFSI investment committee” (see Figure 1 below) to some projects that the EIB previously did not want to fund because it considered them too risky, and that will now benefit from the EU guarantee (even though the EIB is currently well capitalised and already benefits from a guarantee of all EU member states through its callable capital). This is also important because it makes it impossible for private investors or governments to inject capital into the “fund,” as was suggested at the beginning. The only thing they can do is participate as co-financiers of the EIB’s EFSI-labelled projects. The Commission’s boasts about the contributions of member states to the plan through their national development banks have to be seen in this light. It is true that this EU-level cooperation between national development banks could result in positive synergies, but the fact that Kreditanstalt für Wiederaufbau (Kfw), Caisse des dépôts (CDC), Cassa Depositi e Prestiti (CDP), Instituto de Crédito Oficial (ICO) and co. will co-finance some EFSI projects should not be seen as additional investment, but as another reshuffling of funds.

Figure 1: Summary of how the Juncker plan is supposed to work

Source: Bruegel

In the best-case scenario, the creation of EFSI would lead to a major change in the way the EIB functions (even if the EFSI assets will never represent more than 10 percent of total EIB assets). The EIB would finally take on more risk, funding high-risk/high-return projects that are not able to secure finance because of the current high risk aversion of investors because of the crisis. Indeed, as noted for instance by Moody’s, the EIB is currently characterized by its “prudent project selection” and invests mainly in very high quality assets, as suggested by the extremely low level of non-performing loans compared to other development banks (representing only 0.02% of total disbursed loans in 2013). The EIB would also accept a less dominant position by agreeing to finance a smaller share of each project to avoid crowding out private investors (currently between one third and one half, the EIB’s share should diminish to one fifth to arrive at the multiplier of 15 assumed by the plan). In addition, the EIB would be junior to its co-financiers in order to really reduce the risks taken by private investors. This would increase the chances of attracting private investors to finance higher risk projects which are unable to secure funding today. In that case, even if the Juncker plan does not turn out to be the major investment plan that the Commission sold to the public, it would at least stimulate a welcome change in the way the EIB works. That said, a simple reminder from the EIB Board of Governors (composed of all the finance ministers of the EU member states) of the Bank’s essential mission to use its resources to address market failures could have been enough to make that change happen, without the need to involve the Commission or the EU budget.

The costs of reshuffling funds

On the funds themselves, two points should be noted. First, the €5 billion EIB contribution from its past profits would have been used anyway to finance new projects. So while there is no cost in using this money to fund EFSI projects, there is no fresh money involved here: it is just a neutral reshuffling of money from one EIB pocket to the other.

Second, the €8bn from the reshuffling of the EU budget will be mainly taken from Horizon 2020 and the Connecting Europe facility – even if the European Parliament eventually managed to reduce their contribution to €5bn (instead of €6bn). The rest will come from the unused margins of the EU budget. As well as giving us an indication of how highly the new Commission thinks of its own programmes, some significant opportunity costs arise from taking money from the EU’s main research and innovation and transport infrastructure programmes, in order to deposit it gradually into a guarantee fund that might or might not be used, so the EIB can be insured against potential losses.

Is the EIB going to play its part fully?

Overall, the adopted Juncker plan relies on some bold assumptions about the EIB’s future behaviour that seriously look like a leap of faith: that the EIB will be able to find additional projects, that it will be able to attract much more co-financiers than usual, that the projects it will finance are more useful than those usually financed by the EU budget to generate growth and employment. The plan is also underpinned by a more general assumption that the EIB will be able to move away from its risk-averse culture to finance high-risk/high-return projects. All of this is indeed possible (in the best of all possible worlds) but the probability that all of this will be achieved does not seem very high, which leads me to think that the Commission, by giving the lead role to the EIB, has taken a huge gamble. The risk for the Commission is that its flagship investment plan will not be the game-changer announced last year and that its impact in terms of growth and employment will be very limited.

Republishing and referencing

Bruegel considers itself a public good and takes no institutional standpoint. Anyone is free to republish and/or quote this post without prior consent. Please provide a full reference, clearly stating Bruegel and the relevant author as the source, and include a prominent hyperlink to the original post.