Blog Post

The implications of the weakening Yen*

The recent trend of the weakening Japanese yen reflects a major policy shift in Japan, following the formation of the government of prime minister Shinzo Abe. While the speed of yen depreciation has been rather fast, the depreciation has not yet even corrected the yen’s appreciation since the global financial crisis erupted. The new inflation target, two percent per year, is not extraordinary. Therefore, the talks about ‘currency wars’ are not justified. The desperate economic situation of Japan warranted a new policy approach, but there are concerns about the effectiveness of the new policy mix. In the coming quarters, both the euro and the Korean won are expected to appreciate, which could increase concerns that the exports of euro-area and Korean companies will be weakened. In particular, it will make it much more difficult for southern European countries to correct their external imbalances.

Summary: The recent trend of the weakening Japanese yen reflects a major policy shift in Japan, following the formation of the government of prime minister Shinzo Abe. While the speed of yen depreciation has been rather fast, the depreciation has not yet even corrected the yen’s appreciation since the global financial crisis erupted. The new inflation target, two percent per year, is not extraordinary. Therefore, the talks about ‘currency wars’ are not justified. The desperate economic situation of Japan warranted a new policy approach, but there are concerns about the effectiveness of the new policy mix. In the coming quarters, both the euro and the Korean won are expected to appreciate, which could increase concerns that the exports of euro-area and Korean companies will be weakened. In particular, it will make it much more difficult for southern European countries to correct their external imbalances.

Recently-elected Japanese prime minister Shinzo Abe has declared war on deflation, using the heavy armament of fiscal stimulus and monetary easing. His moves have given rise to much controversy, prompting disapproval from policymakers in Europe, Korea and even from China. Indeed, the speed of the yen’s fall was remarkable: by mid-February 2013, the USD/JPY exchange rate jumped to 94, shedding about 21 percent from 78 in September 2012. During the same period, the decline against the euro was 26 percent from the rate of 100 to 127, and 24 percent against the Korean from the rate 0.070 to 0.086.

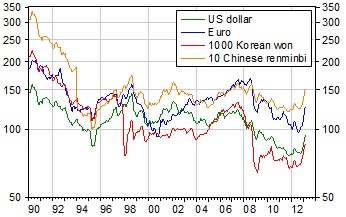

But before claiming that Japan has entered a ‘currency war’, ie an attempt to artificially depreciate the yen in order to foster exports at the expense of trading partners, one has to put into perspective the exchange rate level of the yen. Compared to the pre-crisis period, the 12 February 2013 yen exchange rates were still stronger in nominal terms: between 2004-07 the average rate against the US dollar was 113, against the euro 145, and against the won 0.113. The yen appreciated abruptly after the collapse of Lehman Brothers (Figure 1) and while the recent depreciation was sharp, it has not yet corrected the preceding appreciation.

Figure 1: Japanese yen exchange rates, January 1990 – 12 February 2013

Note: monthly averages up to January 2013; the 12 February 2013 rates for February 2013. A lower value indicates a stronger yen.

Certainly, the real effective exchange rate (REER), which is calculated against several trading partners, and which controls for the differences in inflation, matters more than the nominal rate. Since the cumulative change in the consumer price level was a mere half percent from 1992-2012 in Japan, but 63 percent in the U.S and 106 percent in Korea, there is a major difference between nominal and real exchange rate changes for Japan. Figure 2 shows consumer prices index-based REER developments from 1980 to February 2013. While the most recent value of the Japanese REER is about 14 percent below the average of the past 33 years, the US dollar is also below its historical average by 11 percent, the Korean won by 9 percent and the Chinese renminbi by 7 percent. Only the euro is almost at the historical average (1 percent below the average). And the historical average is not the best benchmark: economic theory predicts real effective appreciation in countries that grow faster than their trading partners, such as Korea and China. Conversely, countries that do not catch-up or even fall behind, such as Japan and the euro area, should see a gradual fall in their real exchange rates.

Figure 2: CPI-based real effective exchange rates, January 1980 – February 2013 (December 2007=100)

Note: the source for January 1995-February 2013 is the updated dataset of Darvas (2012a). I projected the not-yet available consumer price index data by assuming that the 12-month inflation has remained unchanged since the latest available observation. The monthly average exchange rate data for February 2013 is calculated using the actual daily data for 1-11 February 2013 and by assuming that the nominal exchange rates remain unchanged at their 11 February 2013 values till the end of the month. In the pre-1995 period, the OECD’s REER for the US, Euro area, Japan and Korea, and the IMF’s REER for China are chained backward. A lower value indicates a weaker domestic currency.

Therefore, by mid-February 2013, the recent depreciation of the yen largely corrected an earlier over-valuation and therefore talks about a ‘currency war’ are not justified.

There were some good reasons for a change in Japan’s macroeconomic policies. The economy has hardly grown during the past two decades: the cumulative real economic growth in Japan was a mere 22 percent from 1990 to 2012. In contrast, China grew by 761 percent during the same period, Korea by 201 percent. Even the euro area (39 percent), the United Kingdom (57 percent) and the United States (69 percent) significantly outperformed Japan.

Also, in September 2012, Japan’s current account recorded deficits on a seasonally-adjusted basis for the first time since the oil shock of March 1981. While this may be temporary due to the impacts of the territorial spats with China and the spike in imports due to a release of the new iPhone 5 model, the trend is nevertheless worrying. In the longer run, an ageing Japanese population is expected to put pressure on current account deficits and weaken the yen, even if elderly people sell their overseas assets and bring their receipts back to Japan, which would slow the downward pressure on the yen (see Park, 2012).

Therefore, a change in policies was justified, though there are questions about the suitability of the full package. On the monetary front, the new government put pressure on the Bank of Japan (BoJ) to increase the inflation target, which it actually did: in January 2013 the BoJ raised its inflation target from 1 percent to 2 percent. There was much criticism of this pressure from the government, shaming it for exercising undue political influence over the central bank. However, it is the legitimate right of national governments to define the target of the central bank and what is crucial is to respect the operational independence of the central bank. This was respected and a 2 percent inflation target can hardly be assessed as outrageous: in fact, 2 percent inflation is generally regarded as a suitable measure of price stability in advanced countries.

So far, the Bank of Japan has remained reasonably cautious concerning the deployment of new tools: nothing new was announced for 2013, and the potentially ‘open ended’ new asset purchases that will start in 2014 would lead to less than one-third of the increase in BoJ asset holdings in 2014 compared to 2013. Also, this ‘open ended’ 2014 programme largely concentrates on short-term treasury bills, which are to expire shortly. This is the reason why several commentators question the potential for reaching the new inflation target in the near future (excepting a temporary rise in inflation due to the scheduled increase in value added taxes). Certainly, while the incumbent BoJ Governor Mr Shirakawa may be reluctant on significant monetary easing, his term expires this April, and those of his two deputies run out in March. With these changes to the guard, the policy stance of the BoJ Policy Committee may change markedly and more significant monetary stimulus may come.

While I assess positively the decision on the increase of the inflation target and also the recent correction of previous significant over-valuation of the yen, the intended fiscal policy measures raise more questions. Japan’s gross public debt was 237 percent of GDP in 2012, while the net debt was 135 percent of GDP, and another round of fiscal stimulus may increase these ratios further, even if nominal GDP growth speeds up due to monetary measures. So far the Japanese government has not faced problems over new borrowing, which continues to carry ultra-low interest rates, but this may not be the case forever and therefore fiscal policy measures should be cautious.

Monetary policy measures in Japan, but also in other advanced countries, have an impact on emerging countries. If the central banks of major economies adopt expansionary monetary policies and global financial markets become more stable as a result, yen-carry trade (Darvas and Park, 2012) might be revitalised, backed by ample liquidities and ultra-low interest rates in Japan. Recently, net sales positions on JPY/USD futures at the Chicago Board of Trade increased to the highest amount since the global financial crisis (Figure 3), hinting at a future growth in yen-carry trade and not just relative to the dollar, but also relative to the currencies of emerging countries. If the US economy recovers faster than expected this year, the interest rates will rise and the depreciation of the yen might be more significant than the current outlook.

Figure 3: Net Sales Position on JPY and JPY/USD Exchange Rate, January 1993-January 2013

Note: Non-commercial yen net sales position on JPY/USD futures at CBOT

Source: Bloomberg

If the Japanese yen weakens while the Korean won strengthens, Korean companies’ export conditions might take an unfavourable turn, or in other words, the advantage they had since the Lehman Brothers collapse will disappear (Figure 1). A combination of a stronger won and a weaker yen would undermine the export conditions of Korean businesses. Japanese firms have gone through extensive reforms to survive the strong currency, and their aggressive exports based on advanced technologies and overseas relocation of production could damage Korean firms. On the other hand, the weakening yen would relieve the debt burden of borrowers who took out loans in yen.

Japanese monetary policy may also have repercussions on the adjustment in southern European countries. While the European Central Bank resists calls for further interest rate cuts and quantitative easing, other major central banks, including the BoJ, take this route and thereby the euro could appreciate further. A stronger euro would weaken the already fragile European economic recovery, but even more importantly, it would make the adjustment of external imbalances of southern euro-area members extremely difficult, if not impossible, as I argued in Darvas (2012b).

*This article builds on Park (2012) and Darvas (2013).

References

Darvas, Zsolt (2012a), ‘Real effective exchange rates for 178 countries: a new database’, Working Paper No. 2012/06, Bruegel

Darvas, Zsolt (2012b), ‘Intra-euro rebalancing is inevitable but insufficient’, Policy Contribution 2012/15, Bruegel

Darvas, Zsolt (2013), ‘Yen at war’, 25 January, Bruegel Blog

Darvas, Zsolt and Haesik Park (2012), ‘Prospects for the yen carry trade’, EU-Korea Economic Exchange Issue 1, page 6-9, Bruegel and KIF.

Park, Sungwook (2012), ‘The Background and Policy Implications of the Weakening Yen,’ Weekly Financial Review, Vol. 21 No. 47, December 8, 2012, Korea Institute of Finance.

Republishing and referencing

Bruegel considers itself a public good and takes no institutional standpoint. Anyone is free to republish and/or quote this post without prior consent. Please provide a full reference, clearly stating Bruegel and the relevant author as the source, and include a prominent hyperlink to the original post.