Blog Post

Risking their health to pay the bills: 100 million Europeans cannot afford two months without income

Nearly 100 million people in 21 EU countries do not have enough savings in their bank accounts to meet two months of basic expenses: food, utilities, rent or mortgage. Those born outside the EU are especially at risk. Government support is thus fundamental to help individuals withstand the COVID-19 crisis.

Despite state support, the COVID-19 crisis is wreaking havoc on households’ finances across Europe. Millions of individuals have stopped working or had to substantially reduce their working hours because of health restrictions or suppressed demand. How many households in Europe could live without income for one or two months?

In a working paper, we used the 2017 wave of the European Central Bank Household Finance and Consumption survey (HFCS) to estimate how many individuals live in such vulnerable households among 342 million residents in 21 countries: Croatia, Poland and Hungary, and the euro area except for Spain.[1] The methodology section below provides details on the population considered.

Ability to afford food and utilities

According to our estimates, without privately earned income, 29.6 million individuals would be unable to afford one month’s supply of food at home and payment of basic utilities (8.7% of the population considered). This number climbs to 41.6 million for a period of two months without privately earned income, or 12.2% of the population considered.

When taking home 50% of their gross privately earned income, the number of vulnerable individuals decreases substantially to 4.4 million for a period of one month, and 5.5 million (1.6%) for a period of two months.

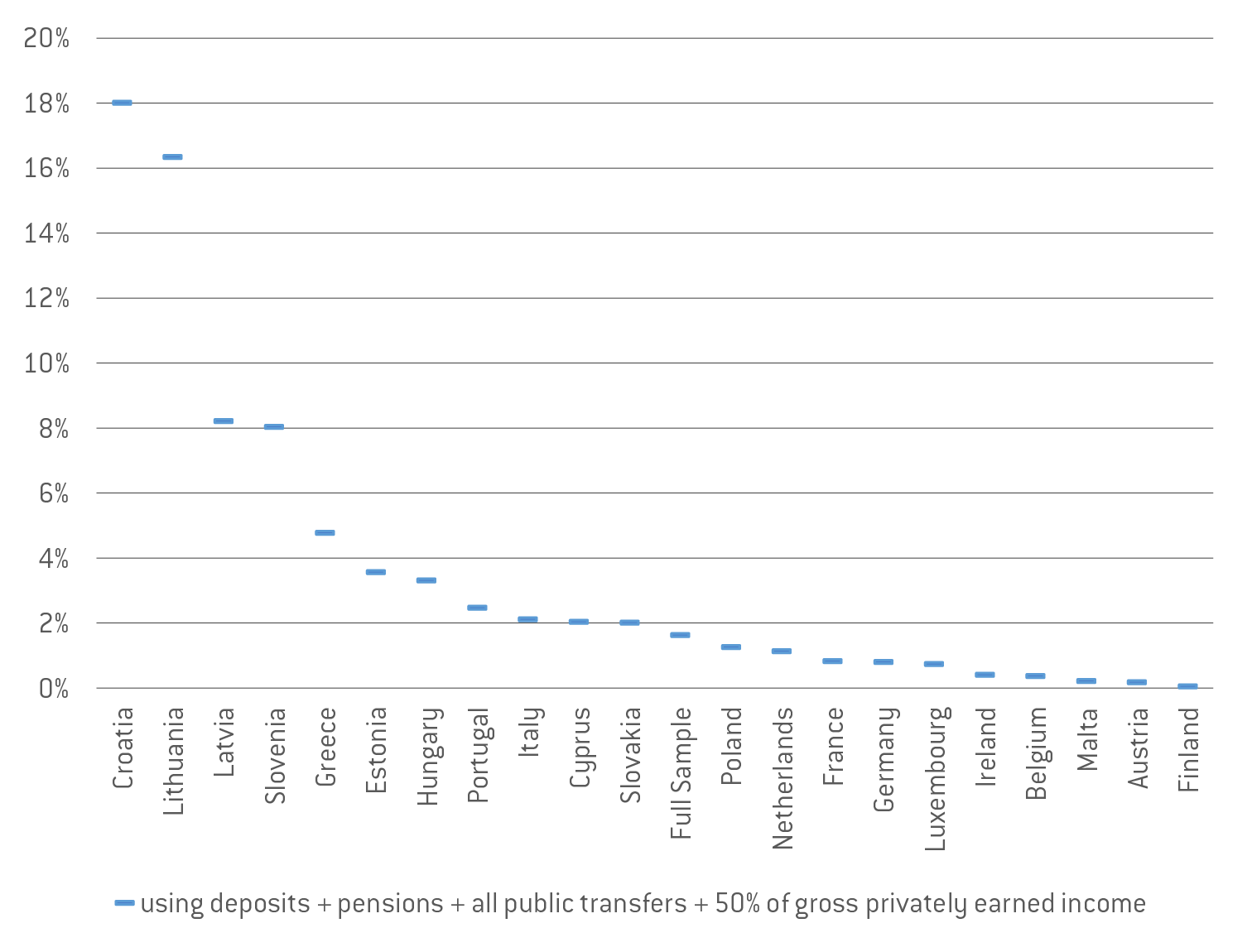

Differences across countries are substantial. In Slovenia, Lithuania, Latvia and Croatia more than 8% of individuals are unable to meet expenses with 50% of their gross income for two months, while in Belgium, Austria, Finland and Malta, less than 0.5% of individuals are in such vulnerable positions (Figure 2).

Figure 1: Percentage of individuals who cannot afford food and utilities for two months with 50% of gross privately earned income

Note: Only individuals living in households with bank accounts were considered.

While percentages allow comparisons between countries, absolute numbers are also relevant. For example, only 2.1% of the individuals considered in Italy are vulnerable when taking home 50% of their gross privately earned income. However, Italy has the highest absolute number of vulnerable individuals: 1.2 million[2]. Germany, Croatia and France follow, all with over half a million vulnerable individuals (see Figure 6 in the annex).

Although numbers decrease when taking precautionary cash savings into account, 1.03 million individuals remain at risk in Italy, and 482,000 in France according to our estimates (see Figure 6 in the Annex).

The relative importance of savings, pensions, public transfers and income

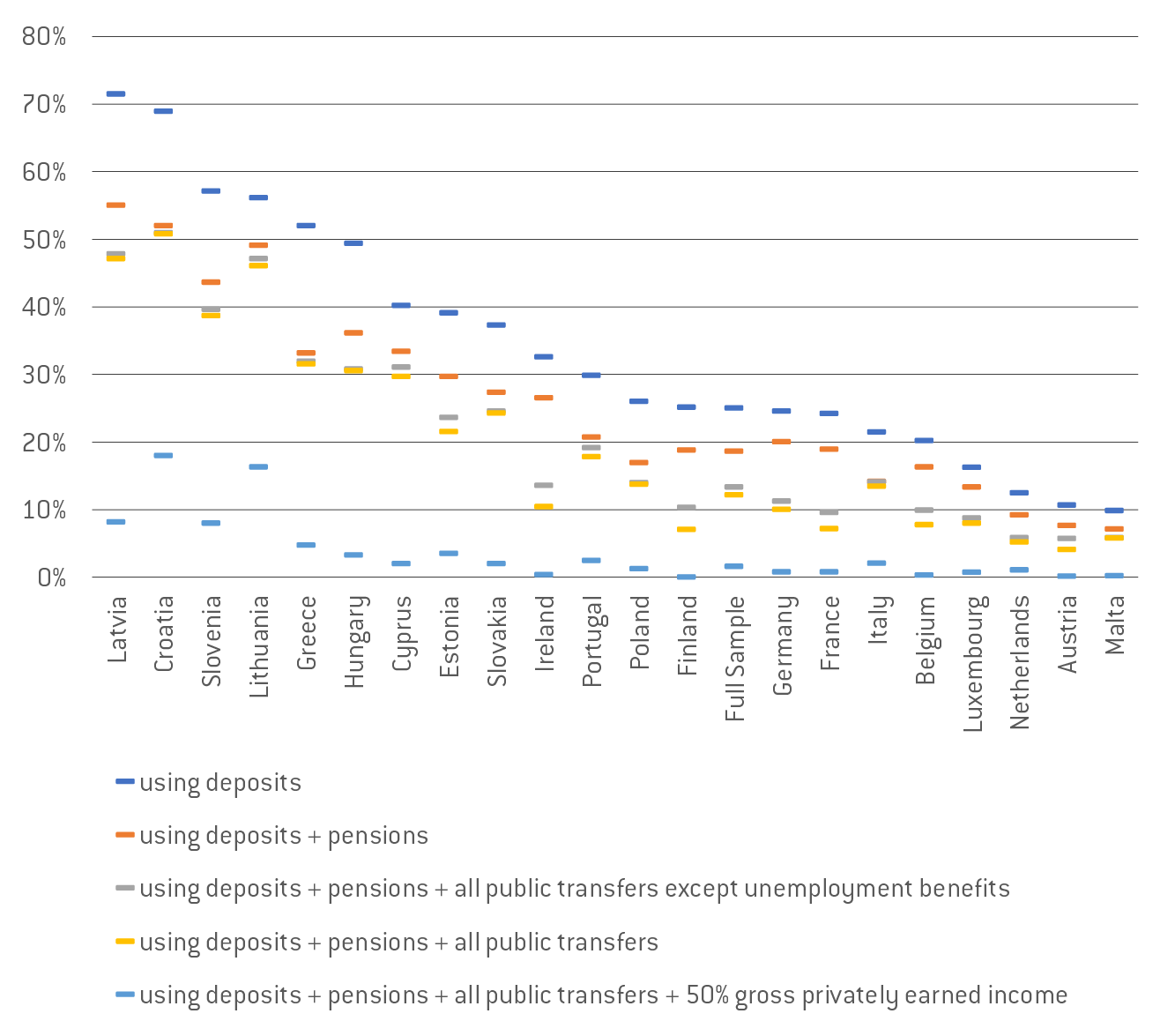

Private income is clearly an essential lifeline for many individuals in the countries analysed. Within one month without privately earned income, 8.7% people cannot afford food and utilities. Within two months the percentage climbs to 12.2%. It is highly variable across countries: below 6% in Malta, the Netherlands and Austria; above 30% in Greece, Slovenia, Latvia, Lithuania and Croatia. (see Figure 4, series ‘using deposits + pensions + all public transfers’).

If we exclude pensions and public transfers and look exclusively at money available on individuals’ bank deposits, we find that 25% of individuals in the countries considered cannot afford food and utilities after two months without income, and 17.4% within the first month. Differences between European countries are striking: in Latvia, 71% do not have large enough bank deposits to face two months of basic expenses, while in Austria and the Netherlands, the percentages are 11% and 12.5% respectively.

Figure 2: Percentage of individuals who cannot afford two months of food and utilities under different income shocks

Note: Unemployment benefits are included in all public transfers. Note: Only individuals living in households with bank accounts were considered.

We also find that:

- Pensions are a fundamental source of income in all countries and substantially reduce the number of vulnerable individuals.

- Public transfers (other than pensions) are crucial in France, Ireland, Finland and Germany. In Italy, Greece and Portugal, they do not provide substantial added social protection beyond pensions.

- Unemployment benefits are particularly important in Finland, Belgium and France.

Housing expenses

Let’s now broaden our definition of ‘basic expenses’ so that), in addition to food and utilities, it includes rent or mortgage on the main residence (for people who own no other residence. With this definition, the number of vulnerable individuals doubles (i.e., those who cannot afford for two months of expenses with 50% of their gross privately earned income double) (Figure 3).

After two months without income, 57.5 million individuals (or 16.8% of the population considered) would not be able to pay their basic expenses from their bank savings, pensions and pre-COVID-19 public transfers. 41.1 million individuals are already in this situation after one month without income.

If 50% of the gross privately earned income is guaranteed, numbers reduce considerably: 8.4 million people cannot meet one month of basic expenses; 11.3 million for a period of two months.

Both rent and mortgage expenses increase substantially the number of vulnerable individuals, but tenants are in the overall sample more vulnerable than mortgage holders. When we considered only utilities and food at home, we found that 5.5 million individuals could not afford two months of expenses with 50% of their privately earned income. Once we add rents on main residences, the number of vulnerable individuals almost doubles to reach 9.8 million. Once we add mortgages on main residences, the number increases to 11.3 million. Rent and mortgage suspension can therefore offer effective support to vulnerable households.

Landlords might be harmed by rent suspension: we estimate 220,000 landlords would not be able to cover their expenses for two months without rental income. Yet, this group is substantially smaller than the 4.3 million individuals who, through a rent suspension, would become able to handle two months

Such measures can be particularly effective in specific countries. While only 0.8% of the French population cannot afford a month of food and utilities, the number quadruples to 3.1% if rents and mortgages are included in the definition of ‘basic expenses’. In Finland, the percentage of vulnerable individuals jumps from 0.1% to 0.5%, and in Belgium, from 0.4% to 1.8%. Such measures would also be highly beneficial in Germany, Ireland and Cyprus.

Migration background

We find that individuals born outside of their country of residence, particularly those born outside of Europe, are substantially more at risk of not being able to afford basic expenses.

Individuals living in their country of birth have a 16.3% risk of not being able to cover basic expenses for two months with no privately earned income. The risk is at 24.7% for those born elsewhere in the EU, and 29.6% and for those born outside Europe. Individuals born elsewhere in the EU are 1.5 (24.7 / 16.3) times more at risk, while individuals born outside the EU are 1.8 (29.6 / 16.3) times more at risk.

Individuals born outside the EU are always at greater risk in all countries except in Portugal and Slovenia[3]. The group born abroad is very diverse, since countries receive not only individuals from abroad from working age but also individuals whose parents had immigrated themselves and retirees from other countries.

Despite those differences, significant migrant groups might also be even more susceptible to higher private income shocks linked to COVID-19 because of precarious labour conditions and prevalence of informal work which hinders access to social security and thus to government assistance policies in the case their income falls.

Conclusion

Resilience to income shocks is highly differentiated across the 21 EU countries analysed. Pensions are an important buffer for households who receive them. The effect of other public transfers is more heterogeneous, having little effect beyond pensions in reducing the number of vulnerable individuals in some countries, namely Portugal, Italy and Greece, but playing an important role in France, Belgium or Germany.

The stark differences in vulnerability might explain different perceptions of urgency and hinder EU cooperation. Measures such as mortgage and rent deferrals are generally helpful to support people in need, though to what extent depends on country characteristics. Policies on rent should safeguard tenants without jeopardising the livelihoods of landlords. Such measures appear feasible, since an income shock threatens the livelihoods of substantially more tenants than landlords.

Providing substantial income support is fundamental even in the very short term, since 57 million individuals cannot meet their most basic expenses from savings, and (pre-COVID-19) pensions public transfers within only two months. Importantly, even when COVID-19 policy responses are in place, namely rent and mortgage deferrals and employment protection schemes, there might still be pockets of vulnerability. Individuals born outside of their country of residence, and especially outside the EU, are a particularly vulnerable group, possibly more likely to suffer income shocks and with limited access to social assistance in the case of income downfall.

For some individuals, the shock we have simulated might be in line with COVID-19 employment protection schemes. For instance, in France and Belgium schemes cover 70% of gross salaries and in Portugal 66%, on which individuals pay social security contributions and income tax. Importantly, schemes provide minimum amounts such as the minimum wage, which ought to decrease the number of vulnerable individuals. In future work, measures can be considered country by country to provide estimates of by how much current policies might have reduced vulnerabilities.

Different levels of vulnerability will translate to different levels of health risk, particularly as countries start relaxing social distancing and allowing companies to return to normal. Individuals who are dependent on their incomes will be forced to leave their homes and resume work earlier, taking greater health risks than they might otherwise choose.

Methodology

In this blog post we set out two scenarios: living without privately earned income and living with 50% of gross privately earned income[4]. For each scenario, we estimate whether households can cover their typical basic monthly expenses (utilities and food consumption at home) by using their bank deposits and their pre-COVID-19 pooled monthly pensions and pooled public transfers[5]. The numbers reported are estimates of the number of individuals living in households that cannot meet these expenses.

Our second scenario postulates government support that guarantees individuals take home 50% of their gross privately earned income. This is more generous than it might at first seem since we are dealing with gross incomes. Regardless of the COVID-19 shock, individuals pay social security contributions and income tax.

We extend the analysis to include monthly mortgages and rents on main residences, but only for individuals who own no other residences. We discuss whether COVID-19 policy measures can ensure the livelihoods of individuals.

The analysis is based on the third wave of the European Central Bank Household Finance and Consumption survey (HFCS), conducted in 2017, which covers 21 countries: Croatia, Poland and Hungary, and the euro area except for Spain[6]. The survey provides information on households and individuals[7].

The survey does not provide information on precautionary savings individuals might hold in cash instead of in bank accounts. We restrict the analysis to households who own bank accounts, as they are more likely to use their accounts as their main source of savings. As a sensitivity analysis, we use a different ECB survey to simulate cash resources, which we add to individuals’ available savings[8].

References

Esselink, H. and L. Hernández (2017), ‘The use of cash by households in the euro area’, ECB Occasional Paper Series No. 201, available at: https://www.ecb.europa.eu/pub/pdf/scpops/ecb.op201.en.pdf

Annex

Figure 4. Thousands of individuals who cannot cover two months of basic expenditures (food at home and utilities) with 50% of their gross privately earned income, by country

A. With deposits, pensions and public transfers

B. With deposits, pensions, public transfers and simulated cash savings

[1] Data on Spain will only be available later in the year.

[2] The number is slightly below 2.1% of the Italian population because we are only considering households with a bank account and because the survey is representative of households and not of individuals directly, though household composition is considered in the sampling design.

[3] We have only considered countries for which they were more than 100 sampled individuals born outside of Europe and more than 100 sampled individuals born in the EU but outside the country.

[4] By privately earned income, we refer to income other than pensions and public transfers. It encompasses salary income, self-employed income, rental income, income from financial assets and regular private transfers.

[5] Utilities comprise electricity, water, gas, telephone, internet and television.

[6] Data on Spain will only be available later in the year.

[7] The HFCS represents the total number of households in each country, not the total number of individuals, but does consider household composition in its sampling design. As result, there are (small) differences in the number of individuals represented in the survey and the number of individuals of the country.

[8] For simulations, we use data from another ECB survey (Table 5 from Esselink and Hernandez (2017)). Table 5 provides percentages of individuals in different precautionary cash savings brackets, by country. We have allocated cash savings randomly among all individuals aged 18 or above to match the country percentages. Individuals randomly assigned to each bracket of precautionary savings in cash were allocated the midpoint of the interval. Individuals assigned to the bracket ‘above 1000’ were assigned 1500 euros. ‘Refusal to answer’ percentages were distributed in proportion of the respondents’ brackets.

Republishing and referencing

Bruegel considers itself a public good and takes no institutional standpoint. Anyone is free to republish and/or quote this post without prior consent. Please provide a full reference, clearly stating Bruegel and the relevant author as the source, and include a prominent hyperlink to the original post.