Blog Post

Chart of the week: Real interest divergence weighs on growth

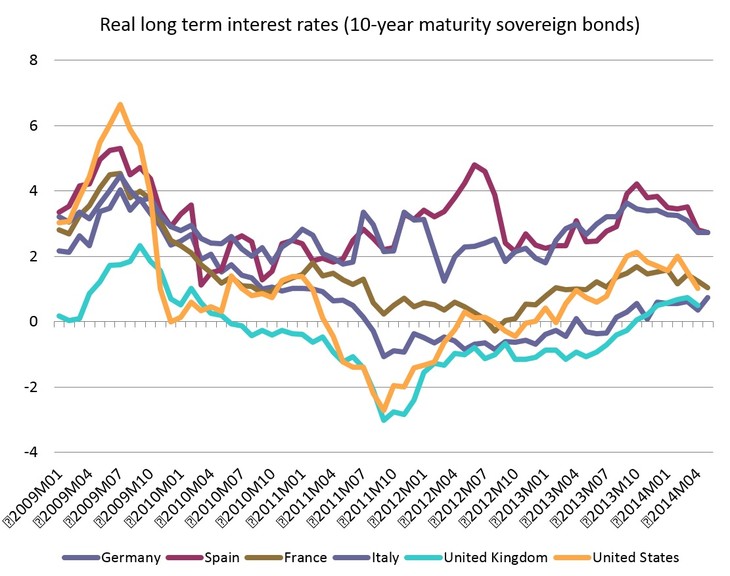

The real interest rate divergence in the Euro Area has recently generated new attention. Real interest rates fell quite substantially in the crisis up to the end of 2011, but have been rising since then. Economic theory would suggest that persistent divergences in such real rates should have had an effect on economic growth performance.

The real interest rate divergence in the Euro Area has recently generated new attention. Real interest rates fell quite substantially in the crisis up to the end of 2011, but have been rising since then (see graph). However, there have been substantial differences across countries, which can be explained by differences in nominal interest rates as well as by diverging inflation rates.

Source: Datastream ThomsonReuters

Note: Real long term interest rates calculated by subtracting HICP rates (all items) from 10-year maturity sovereign bonds.

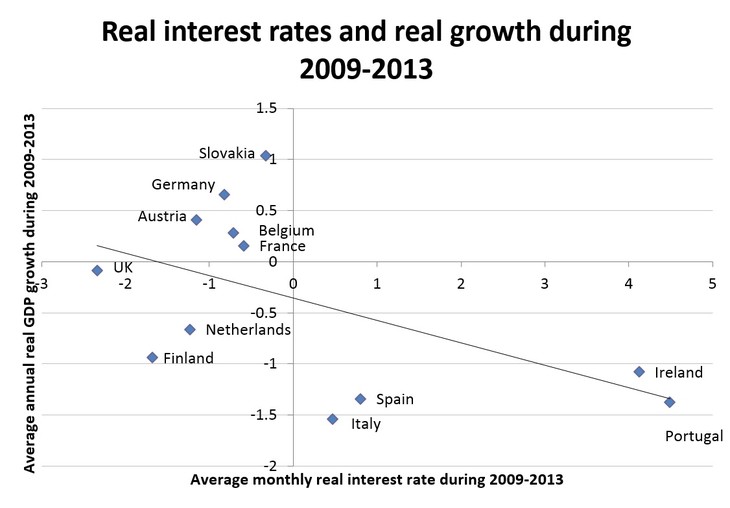

The four countries with the highest real interest rates evidently had the lowest real GDP growth over the crisis years

Economic theory would suggest that persistent divergences in such real rates should have had an effect on economic growth performance, and the chart below suggests that indeed is the case. The four countries with the highest real interest rates (Spain, Italy, Ireland, Portugal) evidently had the lowest real GDP growth over the crisis years. Such a simple correlation obviously should not be interpreted as proof of causality, and other factors certainly have played an important role in explaining the lacklustre performance of the four economies. Yet, the fact that real interest rates have also moved into negative territory in Germany and the UK may suggest that lower interest rates facilitate greater opportunities for growth.

Source: Datastream ThomsonReuters

Note: Average monthly real interest rate calculated with same HICP data as above subtracted by 2-year treasury bond yield data. Both indicators measured a percentages.

Special thanks to Pia Hüttl for her contributions.

Republishing and referencing

Bruegel considers itself a public good and takes no institutional standpoint. Anyone is free to republish and/or quote this post without prior consent. Please provide a full reference, clearly stating Bruegel and the relevant author as the source, and include a prominent hyperlink to the original post.