Blog Post

Can the European Central Bank control interest rates?

The short answer is a hesitant yes, bordering with a timid no.

The short answer is a hesitant yes, bordering with a timid no.

The longer answer starts by noting that the mechanism transmitting the monetary policy impulse from the European Central Bank to the economy is, in essence, a chain with three links: first, the official rate(s) of the ECB; second, the rate at which banks fund themselves, i.e. the funding rate; third, the rate at which banks lend to the economy i.e. the loan rate. In normal conditions, moving the official rate produces well-behaved changes in the other two rates and the central bank has a good handle on the cost at which banks fund the activities of households and firms. In crisis conditions, as often emphasized by the ECB, the transmission mechanism is impaired and the link between the official rate, at one end of the chain, and the loan rate, at the other end, is weaker and noisier. In this blog, the attention will be concentrated on the relationship between the official rate and the funding rate. The analysis of the equally important relationship between the latter and the loan rate, which is influenced by bank behaviour and in particular by the on-going deleveraging process, is left for another time. Suffices it to say here that the uncertainty about this relationship adds to the difficulty of the ECB in controlling the loan rate, which is the most important for the real economy. Add, as the experience of the last weeks vividly showed, the influences on European rates coming from across the Atlantic and you have a full picture.

The funding rate, in the different jurisdictions of the €-area, directly depends on three factors:

- The official rates of the ECB,

- Money market rates, that are influenced by the amount of excess liquidity,

- The pull/push attraction from government yields in the different jurisdictions.

As regards the official rates of the ECB, the President has announced at the beginning of May a cut of the Main Refinancing Operation (MRO) rate by 25 basis points and a cut of the Marginal Lending Rate (MLR) by 50 basis points. At the beginning of June he has reinforced the signal that, if needed, another cut may follow. Of course, the MRO and MLR are directly and precisely under the control of the ECB and their lowering has a direct and positive effect on the funding costs of banks in the periphery of Europe, given that it is predominantly them that borrow from the ECB, while its effect on the banks in the core is very limited, since they already borrow from the market at rates close to zero. Hence the cut of the MRO and MLR rates has an asymmetric effect in the right direction, stronger in the periphery that is recession than in the core, where macroeconomic conditions are distinctly better.

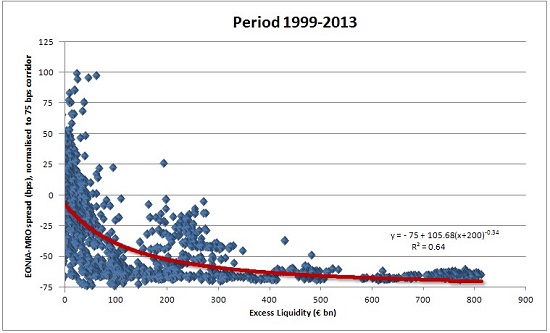

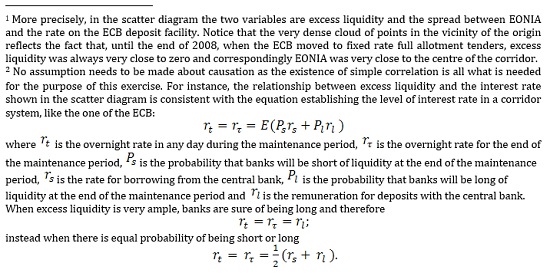

The control by the ECB of money market rates is much less precise than the control of official rates. Indeed these rates depend to a large extent from excess liquidity, which is in turn basically determined by banks’ behaviour, given the full allotment procedure that was recently confirmed to last at least until the summer of next year. In current conditions, given the preponderance of the liquidity provided by the 2 three-year LTRO (78.5% of the total), the development of excess liquidity is dominated by the reimbursement by banks of the borrowings under these operations. These reimbursements are decided, week after week, by banks, comparing the cost (including a stigma effect) of borrowing from the central bank with the cost of borrowing from the market, while giving due consideration to uncertainty and tensions. Between the beginning of 2013, when the reimbursements were first possible, and the 8th of May, when rates were lowered, banks reimbursed about 285 billion, and excess liquidity has come down by some 300 billion, giving a pace of average reduction of liquidity of about 70 billion per month. Since the ECB reduced its MRO rate, the pace of reimbursement has slowed down significantly to some 30 billion per month. Given these developments, excess liquidity remains very large at around 260 billion and EONIA has not moved away from its very low level just a few basis points above zero (we refer to latest ECB data on daily liquidity conditions). On the basis of the relationship between excess liquidity and the EONIA rate[2] shown in the scatter diagram below, EONIA should not move away from that level until excess liquidity will be further reduced towards the 100 billion level.

Chart 1– EONIA spread and excess liquidity since January 1999

However, when that level will be reached, EONIA will start moving up quite steeply and that behaviour could be anticipated by forward interest rates (either Overnight Index Swaps or Euribor rates): interest rate expectations, and therefore forward interest rates, will go up when excess liquidity will be expected to go down, and vice versa.

It is interesting to exploit the strong correlation[3] between excess liquidity and Eonia rate present in the scatter diagram above to estimate, first, what would be the level of forward EONIA rates implicit in some assumption about excess liquidity and, second, using the relationship in reverse, what are the expectations about excess liquidity implicit in current forward EONIA rates.

The exercise of projecting interest rates from assumptions about excess liquidity shows, for example, that, if banks had continued to reduce their demand of liquidity from the Eurosystem at the same average pace of the first 4 months of 2013, EONIA would have reached the MRO rate (or even somewhat above) around September 2013, as excess liquidity would have gone down to zero in that month. This means that EONIA would have moved from the level of a few basis points up to the level of the MRO rate (75 basis points at that time) bringing about an endogenous tightening of monetary policy equivalent to 3 quarter point increases of the policy rate, as anticipated in a previous assessment of the news from Brussels and Washington. However, with the rate reduction (and the expectation that there could be a further reduction), the pattern of reimbursements has, as mentioned above, significantly slowed down. Assuming that the pace of reimbursement of excess liquidity will continue to be lower by about 50% with respect to the average realized until the beginning of May, the ECB would have obtained with the cut of the MRO rate not only cheaper funding for banks but also another four or five months before excess liquidity would go to zero and EONIA would reach the MRO rate, so the move away from 0 would be shifted from Autumn 2013 to Winter of next year. Of course, bringing the MRO rate down to 0.25 would further reduce the cost of central bank borrowing and induce banks to keep a larger amount of excess liquidity, which would keep money market rates closer to zero for even longer.

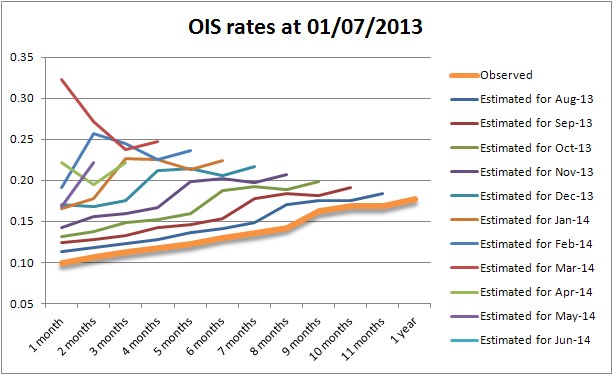

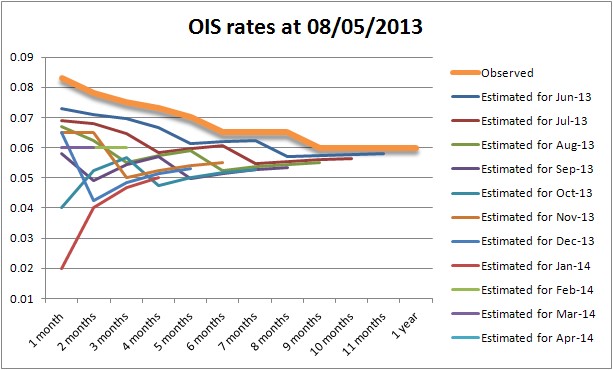

Chart 2 – Implicit OIS rates (%) for the next months at different dates

Sources: Datastream Data and Bruegel computations.

The estimates deriving expectations about excess liquidity from forward EONIA rates observed at the beginning of July (Chart 2, upper panel) indicate that liquidity is expected to remain close to 200 billion until around Spring 2014, as the EONIA curve is fairly flat until then. Notice however in Chart 1 that the relationship between excess liquidity and EONIA becomes noisier as excess liquidity moves towards zero, so the estimate of expected liquidity implicit in forward EONIA rates is not as neat for relative low levels of liquidity. Still, the expectations implicit in forward EONIA rates are overall for liquidity conditions to remain even more abundant than those considered above assuming a reduction of 50% of the drawdown of excess liquidity with respect to what was achieved in the first 4 months of the year. It should, however, be stressed that the EONIA forward curve can change quickly depending on market expectations about the moves of the central bank. Indeed the yield curve of EONIA has already shifted up quite significantly between the day just after the rate cut in May (lower panel of Chart 2) and the beginning of July (upper panel of Chart 2).

In a way, the quantitative exercise reported above measures the potential of “endogenous tightening” that is implicit in the ability of banks to determine the amount of excess liquidity in the system: as the situation improves and banks return the money they borrowed from the ECB, there could still be, with a repo rate at 50 bp, a tightening of the order of 2 quarter point increases that does not derive from any decision of the ECB. Indeed the decision of the ECB to lower rates has pre-empted this potential endogenous tightening: the lower MRO rate directly reduces the potential for EONIA to increase; in addition lower MRO and MLF (Marginal Lending Facility) rates make central bank borrowing cheaper and therefore lower the amount banks will want to reimburse and hence buoy up excess liquidity and keep money market rates closer for longer to the deposit facility rate.

In conclusion, with the cut of the MRO rate the ECB has regained a degree of control on money market rates and excess liquidity, but has far from a precise control.

The influence of the ECB is even less precise and direct on funding rates because of the pull/push attraction from government yields in the different jurisdictions on bank funding costs. The attraction derives from the fact that the yield on government securities acts as a magnet for interest rates in the entire jurisdiction, in particular a bank can not normally fund itself cheaper than the sovereign and will only lend with a mark-up on its cost of funding. The desire and the need to weaken the link between bank funding cost and the yield on government securities is at the basis of the drive towards banking union, but this result is not there as yet and therefore the correlation is still very strong. The pull/push factor is, quantitatively, the most important for funding rates prevailing in individual countries, as the spread between core and periphery bonds, which, for example, is still of the order of 200 basis points for the two year maturity in Spain and Italy, is of course, much more important than the 25 basis point reduction of the repo rate enacted in May and larger of any possible conceivable further reduction of the official rates by the ECB and also larger than the potential “endogenous tightening” estimated above. Still the ECB has some influence on the spreads between sovereign bonds, as shown by the fact that they have come down sharply (of the order of 1700 basis points for Greece, 300 for Spain and 250 for Italy) since the announcement of the Outright Monetary Transaction program last July. However, the spreads are still quite large and this explains, for example, why German banks can fund themselves much more cheaply than Spanish banks (with a spread of 300 basis points). Prospectively, the core-periphery spread will move following the waves of tension/calm in the euro area and does not depend only on the ECB.

The bottom line of this note is that funding rates in the different jurisdictions of the euro area may be buffeted by factors only partially dependent on the ECB, which raises the risk that they would move in a way not fully consistent with the needs of the economy. The concern derived from this conclusion is strengthened observing that the pull/push attraction from sovereign yields will raise bank funding rates in the periphery when the tensions aggravate, thus exercising a perverse monetary tightening. In the opposite direction, one can see a homeostatic reaction at work in the money market because, when the situation gets tenser, banks tend to borrow more from the ECB and this will keep market interest rates low for longer. The contrary will take place when the situation would improve.

The situation in the €-area is different from that in the US, the UK, Switzerland and Japan in two respects. First, the possibility of an endogenous tightening of monetary policy is limited to the ECB and does not extend to the other central banks. In fact all these banks provide liquidity to the market on an outright basis, purchasing securities (FED, Bank of England and Bank of Japan) or foreign exchange (Swiss National Bank), unlike the ECB that provides the bulk of it on a repo basis. The amount of excess liquidity is thus determined in countries other than the euro-area by the central bank, not by commercial banks in their refinancing choices. Second, there is no differential pull-push factor in these countries, in which the rates are dominated by national securities. These differences could be important not only for interest rates but also for the euro exchange rate.

Given the points made so far, one can advance the hypothesis that the ECB lowered its policy rate, may be willing to do this again and announced the Outright Monetary Transaction program not only to lower rates but also to regain at least partial control of funding rates. This adds arguments to the idea that the ECB action is definitely part of its monetary policy responsibility and justifies the hesitant yes given as short answer at the beginning of this blog.

Republishing and referencing

Bruegel considers itself a public good and takes no institutional standpoint. Anyone is free to republish and/or quote this post without prior consent. Please provide a full reference, clearly stating Bruegel and the relevant author as the source, and include a prominent hyperlink to the original post.