Blog Post

Where has all the (base) money gone?

The short answer is: into the liquidity trap.

The short answer is: into the liquidity trap[1].

The longer answer starts from two quotations from Milton Friedman, which give the essence (but not the subtleties) of monetary policy as it stood before the Neo-Wicksellian school concluded that prices, in the guise of interest rate, not quantities, as monetary aggregates, are the alpha and the omega of monetary policy:

1. “…the links between Reserve action and the money supply are sufficiently close, the effects occur sufficiently rapidly, and the connections are sufficiently well understood, so that reasonably close control over the money supply is feasible, given the will.”

(page 89, Friedman, 1960)

2. “No substantial movements in the price level within fairly short periods have occurred without movements in the same direction in the stock of money, and it seems highly dubious that they could. Over long periods, changes in the stock of money can in principle offset or reinforce other factors sufficiently to dominate trends in the price level.”

(Page 86, Friedman, 1960)

Even if the neo-Wicksellian school is in the ascendance, the two ideas in the two quotations have not lost their appeal, for economists and policy makers as well as for the layman[2]. In the first quotation one finds the basic idea that a central bank can control the money supply through the supply of reserves or base (or, more evocatively, high powered) money[3]. In the second quotation one finds the other basic idea that there is a long-term relationship between the development of an appropriately chosen monetary aggregate and inflation.

Still in 2011, one could find a simplified exposition of these two ideas in one of the most popular intermediate macroeconomics textbooks, the one by Dornbusch, Fischer and Startz, surely not economists from a pure monetarist school[4]:

In the textbook, the first idea took the form of the money multiplier, according to which there is a constant, or at least an easy to forecast, relationship between high-powered money and a relevant monetary aggregate. The second idea, which was presented more as an hypothesis than as a demonstrated empirical fact, took the form of a stable demand for money, whereby changes in money market equilibrium are ultimately determined by supply changes decided by the central bank and result, over the long run, in changes in the price level. The practical corollary of the two ideas is that the central bank can pursue price stability, in the medium term, by calibrating the issuance of high-powered money. Friedman even translated this into a simple rule: high powered money should be issued in a way that it would lead to a constant 3 to 5 per cent growth for the relevant monetary aggregate.

In the euro area, empirical facts provided mixed support to these two ideas before the crisis.

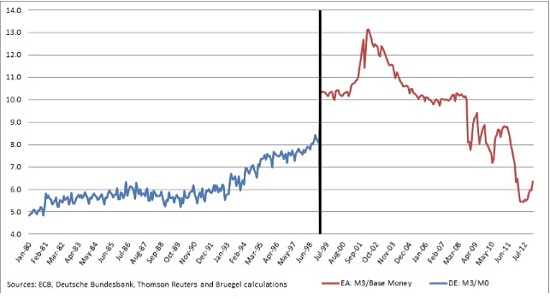

Unlike in the case of Germany before monetary union, in the euro area, the money multiplier only had some kind of stability for a short period between the Autumn of 2005 and the Autumn of 2008. Before that it was affected by the currency change-over, after that by the crisis.

Chart 1 – Money multiplier in Germany (1980-1999) and Euro Area (1999-2013)

As regards the stability of money demand, this was assumed when the monetary policy strategy of the ECB was communicated in 1999: “The available empirical evidence suggests that broad monetary aggregates exhibit the properties required for the announcement of a reference value. […] In the past the demand for euro area broad money has been stable over the long run, [that] empirical evidence has been judged strong and robust enough for a reference value to be announced […]”. (European Central Bank, 1999)

However, subsequent empirical developments did not confirm this statement. Indeed the most exhaustive paper on money and monetary policy of the ECB (Fischer, Lenza, Pill and Reichlin, 2008), which was presented at a conference organized by the ECB, arguably to defend the “Money pillar” in its strategy, concluded that: “…there is no reliable estimated money demand equation which covers the entire sample period”. Still, the paper argued that, a complex, widely judgmental use of monetary variables can help the conduct of monetary policy, including in the forecast of inflation over the medium to long run. Comments made at the conference showed that not every participant to it was convinced of the usefulness of monetary aggregates to forecast inflation, still probably quite a few would have conceded that a central bank should keep an eye on monetary developments in conducting monetary policy. In addition, probably a majority of participants to the conference would have agreed that it is much easier to find a relationship between the growth of monetary aggregates and inflation when both move away from low growth rates, such as those experienced by the euro, to high ones, as happens in the extreme in hyperinflation. This is indeed the idea that Friedman expressed in 1960 when writing that: “While the stock of money is systematically related to the price level on the average, there is much variation in the relation over short periods of time and especially for the mild movements in both money and prices that characterize most of our experience and that we would like to have characterize all.”(page 87, 1960, emphasis added)

During the Great Recession the evidence turned definitely against the two Friedman´s ideas, at least in their simplest, and strongest, formulation.

This was particularly the case for the money multiplier, which was not only unstable, it just disappeared. Two pairs of data suffice to make the point: in the summer of 2009 the 12 month rate of growth of base money was close to 30 per cent, that of M3 was approaching 0; in March 2012 base money was growing at something like 66 per cent, M3 at 3 per cent. A look at the money multiplier itself (look again at Chart 1) shows an instant drop in the autumn of 2008 and wild swings afterwards on an irregular downward trend. A similar development took place in the United States.[5]

Empirical analyses using also data pertaining to the Great Recession (Barigozzi and Conti, 2010) do not manage to get a better empirical relationship between money aggregate growth and inflation. Indeed the two authors reach an analytical and a practical conclusion inconsistent with Friedman´s ideas. The analytical conclusion is that it is “…the role of international financial markets, rather than monetary policy instruments, as the direct determinants of M3 growth rate.” The practical conclusion is that: “ we provide empirical support for a New Two… Pillars Strategy (De Grauwe and Gros, 2009) aimed to achieve financial stability through monetary aggregates and price stability through interest rates.” Hall, Swamy and Tavlas, who also use data including the Great Recession, only salvage the stability of the money demand function introducing, in addition to more standard wealth effects, an uncertainty effect, which of course was particularly strong during the Great Recession. They do not, however, support a return of the ECB to monetary targeting, since the relationship between money aggregates and prices requires interpretation and judgment that can only be pursued in a broadened and deepened monetary analysis.

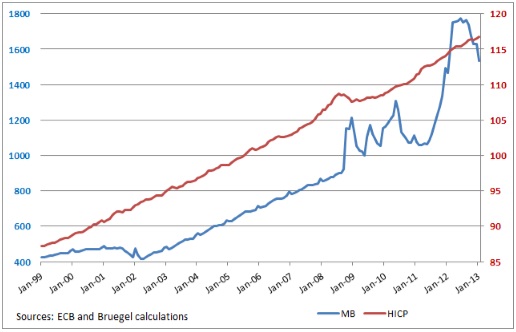

As the joint result of the breakdown of the multiplier and the weak relationship between money and inflation, variations in the base money growth failed to translate into similar variations in inflation[6].

Chart 2 – Monetary Base and Harmonised Index of Consumer Prices in EA (1999-2013)

A central bank wanting to follow the Friedmanian rule and thus stabilize inflation by calibrating base money would have been in deep trouble. Clearly this is not what the ECB has done, given its impeccable control of inflation since it runs the monetary policy of Europe.

The absence of a relationship between base money growth and inflation during the crisis is a fact, but what can explain this fact. In particular, why did the money multiplier break down during the crisis?

A first way to understand the breakdown of the chain linking base money growth to inflation is provided by Woodford: “These familiar mechanisms may have resulted in a fairly reliable connection between expansions of the monetary base and increases in aggregate nominal expenditure under ordinary circumstances — under which a substantial opportunity cost of holding excess reserves exists — but there is no reason to expect them to work in the same way once the opportunity cost is eliminated, because money-market interest rates are no longer higher than the interest rate paid on reserves.”

Basically the Woodford argument is that bank reserves (the relevant part of base money or high powered money) have a special role in facilitating transactions and thus have a well specified demand as long as their interest rate is lower than that on similar assets, but when the interest rate on reserves is the same as on other assets (in particular 0) reserves have no more special transaction role and they are perfect substitute with other assets also yielding 0, their demand becomes perfectly elastic and their size irrelevant for equilibrium.

Another, not inconsistent, way to look at the issue is that base money has lost its “high power” during the Great Recession, because the liabilities issued by the central bank have substituted those issued by commercial banks as the former was forced to bring on its books part of the inter-bank intermediation previously carried out by the private financial market, which was impaired by extraordinarily high credit and liquidity risk: in a way deposits with the central bank and ordinary inter-bank deposits can no longer be distinguished one from the other (Papadia and Välimäki, 2011). A similar point was made by von Hagen (2009), who interestingly noted that it was the “reserve ratio” that increased precipitously during the Great Recession, unlike in the Great Depression, when it was the “currency ratio” that increased and made the money multiplier plummet[7].

Of course, the loss of “high power” by bank reserves opens up an entirely different issue, namely what was the macroeconomic effect of the very large creation of base money and concomitant increase in the balance sheet of central banks during the Great Recession. To put the issue in (too) stark terms, the question is whether the effort of central banks in expanding their balance sheets was in vain. But this is an important issue, which we leave to another blog.

While base money control was irrelevant for inflation control during the Great Recession would this be the case on a permanent basis? The answer is that the control of the central bank balance sheet and of bank reserves in particular, will be important again when the situation will normalize. This is a much weaker statement than saying that a stable multiplier and a stable, standard money demand will prevail after the crisis. There is no need to believe in the latter stronger statement to make the point that the central bank should care about the growth of its balance sheet in circumstances different from the highly exceptional ones prevailing during the crisis: base money control will remain insufficient to control inflation, still it will be necessary, if only to calibrate appropriately interest rates in a neo-Wicksellian approach. This of course stresses the importance of planning for the exit from the exceptionally easy monetary policy that is now prevailing in most of the advanced economies, which is somehow in contrast with the preoccupation of a number of central banks, with the possible exception of the ECB, to postpone as far as possible into the future any idea of normalization of monetary policy.

References:

Matteo Barigozzi, Antonio Conti: On the Sources of Euro Area Money Demand Stability A Time-Varying Cointegration Analysis, ECARES Working Paper 2010‐022

Rudiger Dornbusch, Stanley Fischer and Richard Startz: Macroeconomics, 11th Edition, 2011, McGraw- Hill Irwin, New York

European Central Bank (1999): The Stability-Oriented Monetary Policy Strategy of the Eurosystem, Monthly Bulletin, January, 39-50

Björn Fischer, Michele Lenza, Huw Pill and Lucrezia Reichlin: Money and monetary policy: the ECB experience 1999-2006, in European Central Bank, The Role Of Money – Money And Monetary Policy In The Twenty-First Century, 2008

Milton Friedman: A Program for Monetary Stability, Fordham University Press, New York, 1960

Milton Friedman: The Role of Monetary Policy, American Economic Review, March 1968

Charles Goodhart, Melanie Baker, Jonathan Ashworth, Anthony Obrien, Monetary Targetry: Possible Changes under Carney, UK Economics and Interest Rate Strategy, Morgan Stanley, January 9, 2013.

Stephen G. Hall, P.A.V.B Swamy and George S. Tavlas: Milton Friedman, the Demand for Money and the ECB´s Monetary Policy Strategy, Federal reserve Bank of St.Louis REVIEW, May/June 2012

Francesco Papadia and Tuomas Välimäki: The functioning of the Eurosystem Framework since 1999, In The Concrete Euro – Implementing monetary policy in the euro area,

Paul Mercier and Francesco Papadia eds. Cambridge University Press, Cambridge, 2011

Jürgen von Hagen: The Monetary Mechanics of the Crisis, Bruegel policy contribution, Issue 2009/08, August 2009

John C. Williams: President and CEO, Federal Reserve Bank of San Francisco. July 2, 2012

Monetary Policy, Money, and Inflation

Michael Woodford: Methods of Policy Accommodation at the Interest-Rate Lower Bound, Mimeo, Columbia University, August 20, 2012

[1] This blog can be seen as an update of the Bruegel Policy Contribution of Jürgen von Hagen, who made a very similar point in 2009. Comments by George Tavlas are gratefully acknowledged.

[2] In a recent article, Hall, Swamy and Tavlas argued that the ECB monetary policy strategy has been “considerably influenced” by Milton Friedman´s ideas. Indeed there is still a monetary policy pillar in the ECB monetary policy strategy, even if it seems dormant.

[3] To be precise, base money includes currency in circulation in addition to bank reserves. However currency in circulation is entirely demand determined and the central bank has no direct influence on it, thus the part of base money that is relevant for monetary policy is bank reserves.

[4] Macroeconomics, 11th edition, 2011.

[5] Goodhart and al. describe what happened tot he money multiplier as follows: “… the determined upwards leveraging of Central Banks’ balance sheets has been met and offset by a massive deleveraging of private sector balance sheets, in particular amongst banks.”

[6] Different attempts that we conducted failed finding an empirical relationship between the two variables.

[7] The reserve ratio (r) and the currency ratio (c) determine the money multiplier in the formula: M = (1 + c) / (c + r) B, where M is the money supply and B is base money.

Republishing and referencing

Bruegel considers itself a public good and takes no institutional standpoint. Anyone is free to republish and/or quote this post without prior consent. Please provide a full reference, clearly stating Bruegel and the relevant author as the source, and include a prominent hyperlink to the original post.