Blog Post

Can Europe manage if Russian oil and coal are cut off?

A stop to Russian oil and coal supplies would push Europe into a short and painful adjustment period. But if managed well, disruptions would remain temporary.

While the United States, Canada and the United Kingdom have announced embargoes or phase-out measures for Russian energy in the wake of the war in Ukraine, the European Union has held back, instead launching a new energy strategy, REPowerEU. This aims to reduce by nearly two thirds the EU’s gas imports from Russia by the end of 2022, and to make Europe independent from all Russian fossil fuels well before 2030. Renewables will only be able to play a significant additional role in EU energy independence in the medium term: in the coming months alternatives will need to do the heavy-lifting.

If forced, Europe can manage next winter without Russian gas. But can Europe also sustain an interruption to Russian oil and coal supplies, brought about by either Russia coercion of Europe to extract concessions on Ukrainian sovereignty by threatening energy supplies, or by Europe itself, should governments decide to reinforce sanctions against Russia with an energy embargo?

Market players have already started to limit their Russian coal and oil purchases, either because of the reputational risks or for fear of being caught out by further sanctions. Several energy companies have stopped buying Russian oil, while others buy only at substantial discount to equivalent non-Russian oil grades: on 16 March the discount of Urals compared to Brent was $27/bbl or 24%. The International Energy Agency suggests that 3 million barrels per day (mb/d) of Russian crude oil and oil products may not find its way to markets beginning in April 2022, as sanctions bite and buyers hold off.

Oil

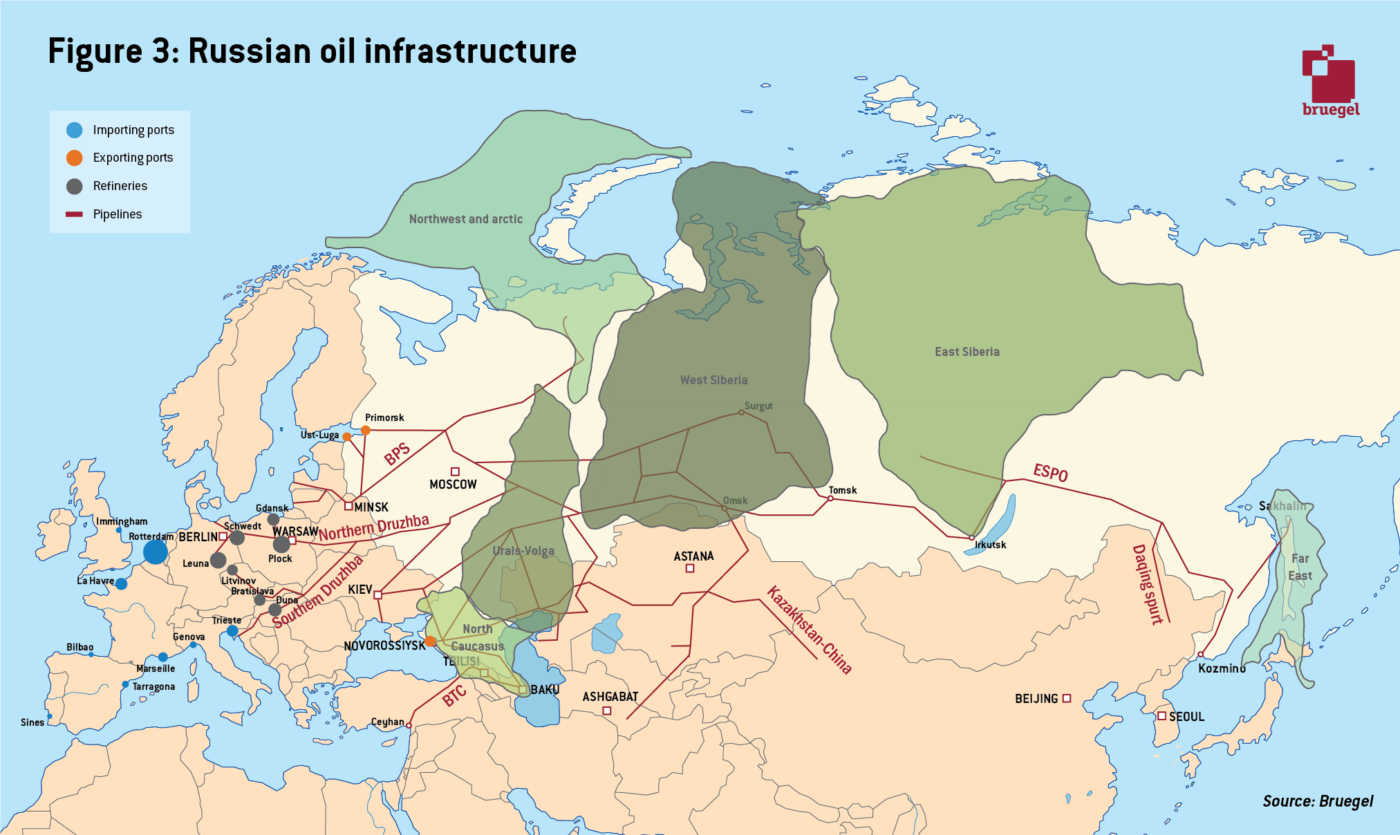

Russia is the world’s largest oil exporter at about 8% of world supply, and the EU the world’s second largest importer, and largest buyer of Russian oil (Figure 1).

Russia: the world’s largest oil exporter

In December 2021 Russia exported 5 mb/d of crude oil and 2.8 mb/d of oil products, including 1.1 mb/d gasoil/diesel, 0.6 mb/d fuel oil, and 0.5 mb/d naphtha. In 2020, total crude exports to Europe were 2.8 mb/d, of which around 0.7 mb/d was by pipeline, with the remainder by sea. Total crude exports to Asia were 2.1 mb/d, with 0.8 mb/d directly to China via pipeline. Over 70% of Russia’s oil product exports went to the European and US markets.

In 2021, crude oil and petroleum product exports made up 37% of Russian export revenue, according to the Federal Customs Service of Russia, when oil prices were on average $71/bbl. In February 2022, the price of Russian oil averaged $92/bbl.

Historically, Russia’s oil infrastructure was built to serve eastern European markets, namely via the Druzhba oil pipeline which directly feeds six refineries in the EU, but since 2009 (when the first phase of the ESPO-1 pipeline was completed), Russia has developed export routes to Asian markets and directly into China.

We estimate that 4 mb/d of Russian crude oil is vulnerable to an oil trade embargo by the EU and other non-European OECD countries (an alternative estimate is 4.8 mb/d). This includes some oil from Kazakhstan, which is interlinked into Russian export routes. More than 1.5 mb/d of oil products flowing to non-European OECD countries are also at risk. Evidence so far suggests that while oil has continued flowing through pipelines, Russia is struggling to find buyers for seaborne shipments, with buyers shunning around 1.6 mb/d of crude and 1 mb/d of oil products, which could become 3 mb/d in April.

The EU: the world’s second largest oil importer

In 2020, the EU imported 9.3 mb/d crude oil and 5.6 mb/d of refined oil products, according to Eurostat. Around 8 mb/d of imported or domestically refined products (Figure 5) is used for transport (diesel, gasoline, kerosene), around 3.5 mb/d for heating (gasoil, fuel oil), and 2 mb/d as a chemical industry feedstock (naphtha, LPG). Some of these fuels are re-exported to markets such as the US and Switzerland.

In November 2021, Russia accounted for just under 30% of the EU’s crude oil imports and just over 15% of oil products. In case of a disruption in Russian supplies, the EU would be most vulnerable in terms of diesel, naphtha and fuel oil.

In 2021, total EU oil imports amounted to 15 mb/d, of which 3.5 mb/d came from Russia, resulting in €88 billion flowing from the EU and the UK to Russia.

Aggregate global oil supply

Were EU-Russian oil trade to stop, around 3 mb/d of Russian crude supply and around 1 mb/d of oil products would be taken offline, constituting a serious global supply shock. With already tight oil markets, it is not clear that suppliers would be able or willing to make up the shortfall.

OPEC spare capacity estimates range up to 4 mb/d. This includes 1-2 mb/d from Saudi Arabia, around 0.75 mb/d from the United Arab Emirates and 0.5 mb/d from Iraq. Iran, currently locked in negotiations on the Iran nuclear deal, which will determine if it can export oil, has about 1 mb/d of spare capacity. Iran has been producing low volumes since 2018, so it is not clear how quickly could ramp up supply. Estimates suggest 0.5 mb/d could come back immediately, with another 0.5 mb/d later in the year.

However, OPEC members currently have an agreement with Russia and Central Asian partners known as OPEC+, under which it has been agreed to constrain supply growth to 0.4 mb/d per month. As long as they don’t boost production, the US and its allies face a difficult question of how much political pressure to exert and where to compromise. The US has already spoken to Venezuela, indicating that Western sanctions on Russia may come at the cost of removing sanctions elsewhere.

In any case, OPEC members seem to be struggling to meet their own production targets. In December 2021, output increased by 0.25 mb/d compared with the target of 0.4mb/d. The situation recently worsened with the loss of 0.3mb/d capacity from Libya.

US production dropped by around 3mb/d at the start of the pandemic, and has gradually clawed back around half of this. The shale industry is in discussions with the US administration on how production can be ramped up. Typically, shale is considered flexible and should respond to high prices. A timescale of 6-12 months for additional capacity seems realistic.

Finally, OECD members hold strategic oil reserves of 1.5 billion barrels. This supply could compensate for at-risk Russian exports for around one year. Industry holdings are another 3 billion barrels. Therefore, an immediate embargo on Russian oil can be partially mitigated by slowly drawing down on strategic stockpiles whilst boosting alternative output. Within the EU, the Oil Stocks Directive (2009/119/EC) requires countries to maintain emergency stocks of crude oil and/or petroleum products equal to at least 90 days of net imports or 61 days of consumption, whichever is higher.

Can Europe replace oil imports from Russia?

The fact that a large share of Europe’s crude oil imports are by ship rather than pipeline means that in principle, replacing Russian oil will be easier than replacing Russian gas. However, three major bottlenecks should be considered:

- i) Intra-European oil infrastructure: if Russian oil supplies stop, it will be challenging to re-route crude oil and oil products inside the EU. The infrastructure is designed for east to west flows, and moving crude oil and products eastwards might entail abnormal movements of crude, including via rail, truck and river barge.

- ii) Refineries: certain European refineries are optimised to use Russian oil and will be less efficient if producing with a different quality of crude. Iraqi and Iranian crude come closest to Russian crude. Particularly vulnerable are six large refineries along the Druzhba pipeline (in Poland, Germany, Czechia, Austria, Hungary and Slovakia). In 2019, these refiners were subject to a stress test as flows were disrupted because of contamination of oil. They passed the test using strategic reserves, crude stored onsite and re-routed seaborne deliveries. But these outages lasted only two months. If it is not possible to feed these refineries, slack will have to be taken up in alternative refineries to meet final product demand. While port refineries are still vulnerable to a drop from such a large supplier, they are typically better placed to: a) accept different crude types, and b) accept consignements from new suppliers.

iii) Replacing Russian refining capacity: beyond crude oil supply, the EU must also consider replacing Russian refining capacity that produces diesel, naphtha and fuel oil. European refiners could try to compensate for this by increasing refinery throughput. To replace lost Russian diesel supply, for example, European refineries would have to raise runs by about 10 percentage points, taking them to almost 90% of total capacity of 15-16 mb/d. It would be the highest utilisation rate this century.

Oil demand reduction

Since it will be difficult for Europe to entirely, and in a timely way, replace Russian crude oil and oil products, governments must encourage demand reduction.

European governments plan or have already adopted an approach of ‘positive discrimination’ by subsidising certain consumer groups exposed to high energy prices. Demand was boosted beyond what typical market forces would have encouraged. In the scenario of no Russian energy, this approach will become excessively expensive and lead to bidding wars for limited fuel. Instead, the focus should be on cutting proactively rather than boosting demand. This will calm markets and allow supply and demand to meet at a more reasonable price.

EU and other OECD countries should swiftly enact coordinated plans to reduce demand. Analogies with actions taken during the Second World War or the 1973 OPEC oil embargo are not far-fetched. International Energy Agency members should maintain a programme of demand restraint measures, to bring about a rapid 10% reduction in oil demand. This would give markets enough time for a structural reorientation away from Russian oil. Every barrel of oil saved now can remain in storage and be available in case of supply disruption.

The most effective demand-side measures for oil will come from the transport sector. Table 1 summarises key points as set out in an IEA handbook on reducing oil demand. Measures that should be considered include encouraging public transport by, for example, making services free on weekends and campaigns to encourage car-sharing by employees, which businesses can be incentivised to support.

In case softer measures fail, stricter measures like restrictions on when certain vehicles can drive may be necessary. Governments should also liaise closely with freight companies to discuss options for route and fuel sharing.

Coal

[1] Europe includes all European members of the OECD and Albania, Bosnia-Herzegovina, Bulgaria, Croatia, Cyprus, North Macedonia, Georgia, Gibraltar, Malta, Montenegro, North Macedonia, Romania and Serbia.

Globally, the main exporters of coal are Indonesia, Australia, Russia, Colombia, South Africa and the United States. On the demand side, China is by far the main consumer (accounting for half of global consumption) and the major importer, followed by India, Japan, Europe[1] and other Asia-Pacific countries.

With gas prices on an inflationary spiral, the price of coal has also picked up, quadrupling in one year. Coal and gas are competitors in the electricity market as they both fill what is known as the ‘thermal gap’: the difference between electricity demand and generation from carbon-neutral energy sources.

The EU market

The EU has been gradually phasing out solid fossil fuels, bringing down consumption from 1,200 to 427 million tons (MT) over three decades (1990-2020). We focus on hard coal, as lignite is produced and consumed domestically. Hard coal consumption and production in the EU has declined, especially in the past few years. In the process, imports have become more significant, from 30% to more than 60% of domestic consumption, raising questions about the availability of hard coal for the EU in case of a major disruption, such as an energy embargo on Russia.

Russia has played a major role in filling the gap between the EU’s consumption of hard coal and domestic production, with EU hard coal imports from Russia rising from 8 million tonnes (MT; 7% of total EU imports) in 1990 to 43 MT (54%) in 2020.

It is important to distinguish between thermal coal, also known as ‘steam coal’, that is used to generate electricity, and metallurgical coal used in iron and steel making. Russian metallurgical coal accounts for between 20% and 30% of the EU’s coal imports, while the Russian share of the EU’s imports of thermal coal is almost 70%. Germany and Poland are particularly reliant on thermal coal from Russia.

Replacing current volumes of Russian coal (>40 MT) might only be part of the challenge. If Russian gas and oil supplies are also stopped, the EU might want to import more coal to produce electricity. In fact, in terms of electricity, the EU has enough spare capacity to drastically increase power generation from coal in case of an emergency. Had all hard coal power plants in Germany operated at full capacity in 2021 they would have produced around 140 TWh more of electricity, consuming about 40 MT of additional coal.

Diversifying and increasing EU coal supply

Though Russian imports make up a significant share of thermal coal consumed in the EU, there are signals from the industry that Russian imports could be replaced relatively quickly. Most prominently, the German association of coal importers has said Russian coal can be substituted in a few months. It is unclear, however, how much of a buffer EU coal stocks would provide for the transition phase. The reported 2.6 million tonnes stocked in ports would cover about three weeks of Russian imports, but more coal should be sitting in the stocks of power plants.

Russian coal can be replaced because global coal markets are well supplied and flexible. It was only Russia’s aggressive push in the past decade for market share in the EU that pushed out other suppliers. In principle, shipments from countries that have reduced exports to the EU are still largely available to substitute for Russian coal. Comparing the maximum yearly global exports of the main exporting countries in the last six years (2016-2021) against their 2021 export levels, there seems to be enough margin to replace Russian global exports of coal almost entirely. If China and India (the two main consumers of coal worldwide) were to buy more coal from Russia, the export margin from other global suppliers may increase further. Similarly, increasing EU domestic production which reached a new low in 2021 (329 MT vs 373 MT in 2019) by some 40 MT might be possible in an emergency.

Clearly, constraints in coal demand and in production by exporting countries may prevent full exploitation of the potential export margin. For example, in January this year Indonesia introduced a temporary ban on coal exports and seems set to do the same in April. On the other hand in Colombia, after a production nose-dive in 2020 (-40%) because of the pandemic and a prolonged strike at a major mine, is set to increase output by 7 MT throughout 2022 after a bounce back in 2021.

Australia’s coal exports in the last year and a half were redirected to India after China introduced an import ban on Australian coal. The Chinese boycott has freed up additional export margin in Australia, given that India has not fully compensated for the loss of the Chinese market. However, Australia is experiencing temporary supply interruptions due to climate change as wildfires and flooding hamper the country’s ability to exploit its export potential to the fullest. The embargo on Australian coal also pushed China to expand its own coal production to produce 220 MT a year extra, a 6% rise from last year.

South Africa also seems to have substantial export margin potential, given that its coal exports in 2021 were at their lowest level since 1996 because of political turmoil and security and operational issues. Richards Bay Coal Terminal, the main coal export terminal in the country, expects exports to rebound in 2022 to 70 MT (a 17% increase).

Finally, in 2022 the US Energy Information Administration (EIA) expects US coal production to increase by more than 25 MT (4%), while domestic consumption is set to decrease by 7 MT. The EIA expects this to support exports while helping replenish coal inventories at power plants.

Replacing Russian coal imports will require the lightspeed deployment of new supply chains to bring the right type of coal to where it is needed. Most European coal users already source from different suppliers and should be able to build on existing relationships. On the policy side, public risk-sharing and diplomatic support might be needed to speed up the process. Moreover, it should be assessed whether some environmental rules should be relaxed temporarily to allow the use of more easily-available coal types.

Higher coal demand, lower coal supply and more complex logistics will increase the cost of coal imports and might lead to temporary local disruptions. However, stopping imports of Russian coal would appear not to cause dramatic supply disruptions on aggregate.

Conclusion

While stopping Russian gas imports would be difficult and costly, but feasible, it will likely be less painful for the EU to manage a complete interruption of Russian oil and coal imports. Oil and coal are more global and liquid markets than gas, and rely less on rigid infrastructure like Europe’s gas import pipelines. However, this implies that a European halt to Russian oil and coal supplies would have substantial global second-round effects. Europe might be hit hard by higher prices, but being a wealthy continent would be able to attract more crude oil, oil products and coal, which might be increasingly difficult for emerging and developing economies.

Europe can manage without Russian oil supplies but significant coordination and logistical problems will have to be tackled. Europe and the US should forge a Trans-Atlantic Energy Pact to make direct and indirect (including fuel switching) spare capacities in the US available to help Europe deal with lost Russian volumes. Joint diplomatic efforts towards OPEC producers would help narrow the gap, which will be done by price-driven oil-demand reduction across the globe. Any short-term deficit can be met by the large oil and product stockpiles, and by activating government plans to reduce demand significantly. A stop to oil imports from Russia will imply higher oil prices for Europe, but global markets will ensure Europe gets all the oil it is willing to pay for, and markets will ultimately rebalance.

On coal, switching European supplies away from Russia while meeting increasing coal import needs will lead to higher global coal prices, again with significant second-round effects on emerging and developing economies. Logistical questions also have to be solved. It is of paramount importance for Europe to quickly buy more coal and replenish its coal stocks, in particular because of potentially higher coal-burn in power plants.

While Europe will go through a short and painful period until demand and supply re-adjust, if these measures are accompanied by a renewed impetus for a transition towards carbon-neutral energy sources then Russia’s leverage over EU energy supplies will disappear.

Recommended citation:

McWilliams, B., Sgaravatti, G., Tagliapietra, S. and G. Zachmann (2022) ‘Can Europe manage if Russian oil and coal are cut off?’, Bruegel Blog, 17 March

Republishing and referencing

Bruegel considers itself a public good and takes no institutional standpoint. Anyone is free to republish and/or quote this post without prior consent. Please provide a full reference, clearly stating Bruegel and the relevant author as the source, and include a prominent hyperlink to the original post.