Blog Post

How have the European Central Bank’s negative rates been passed on?

Negative rate cuts are not that different from ‘standard’ rate cuts. Like them, they reduce banks’ margins, but this effect does not appear to be amplified below 0%.

Since the global financial crisis, several central banks have deployed negative policy rates, after exhausting conventional easing measures. The European Central Bank introduced its negative interest rate policy (NIRP) in June 2014 when it cut its deposit facility rate below 0% for the first time, to -0.1%. Since then, the rate has been cut four more times, by 10 basis points each time, to reach -0.5% in September 2019. After seven years of NIRP and with markets currently expecting rates to stay negative for the next five years, it is crucial to fully understand the effects of prolonged negative rates on the economy.

While those central banks that have adopted NIRP are generally positive about its value in helping them fulfil their objectives, it remains controversial and has been accused of causing significant side effects, particularly in the banking sector. As a result, two major central banks, the US Fed and the Bank of England, have refrained from using it.

In a paper for the European Parliament, we looked in detail at the possible effects and side effects of the ECB’s NIRP. Here, we focus on the transmission of the negative policy rate to bank rates. This is important because a compression of the spread between credit and deposit rates would reduce banks’ net interest margins and possibly their profitability.

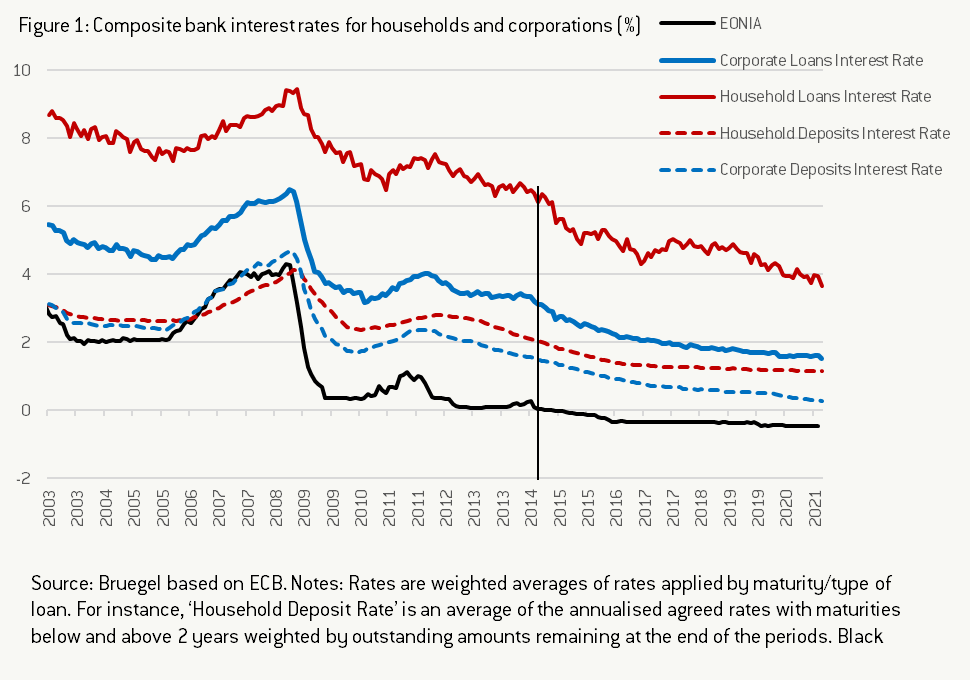

It is difficult to see with the naked eye how policy rates influence bank rates and if the effects change below the zero/effective lower bound (Figure 1), so we investigated with a simple econometric analysis the pass-through from policy rates to bank rates.

We first constructed composite interest rates for household and corporate loans and deposits. Using ECB data, we weighted various interest rates with different maturities and purposes (eg loans for house purchase with a maturity of more than 10 years) by their size relative to their category (other loans made to households). This provided us with the four composite interest rate time series for the euro area depicted in Figure 1.

Next, we explored the relationship between the monetary policy rate (proxied by the EONIA) and these different bank rates. First, we estimated the long-run relationship between the two variables with the following regression:

where ![]() is a given bank rate (eg loans for households) and

is a given bank rate (eg loans for households) and ![]() is the monetary policy rate (proxied here by the EONIA). This first analysis gives a sense of the strength of the relationship between the two variables but does not take into account time trends or measure the speed at which the monetary policy rate has an impact on bank rates. The order of the observations (the months) does not have an impact on the outcome of the analysis (you could shuffle around the months and not change the correlation coefficient). Table 1 summarises the results for all four types of interest rates.

is the monetary policy rate (proxied here by the EONIA). This first analysis gives a sense of the strength of the relationship between the two variables but does not take into account time trends or measure the speed at which the monetary policy rate has an impact on bank rates. The order of the observations (the months) does not have an impact on the outcome of the analysis (you could shuffle around the months and not change the correlation coefficient). Table 1 summarises the results for all four types of interest rates.

These results indicate that the pass-through is incomplete for all interest rates: a 1-point decrease in the policy rate is not translated into a 1-point decrease in banking rates. In addition, the pass-through is significantly greater for rates applied to banks’ assets (loans) than to their liabilities (deposits). Similarly, the pass-through is greater for corporations than for households.

Next, we looked at the short-term effect of changes in the policy rate on bank rates in order to assess whether this relationship has changed since rates have been negative. In the spirit of ECB (2006), we estimated the following regression:

where ![]() This second regression is based on a more traditional time series analysis. We assumed that the change in the bank rate between t-1 and t is explained by the error in t-1; that is to say, the difference between its value and the value predicted by the long-run relationship between the two variables:

This second regression is based on a more traditional time series analysis. We assumed that the change in the bank rate between t-1 and t is explained by the error in t-1; that is to say, the difference between its value and the value predicted by the long-run relationship between the two variables: ![]() . Therefore

. Therefore ![]() , the speed of adjustment (or error-correction coefficient), is expected to be negative: if the banking rate is higher than it should be (as predicted by the long-run relationship), it is likely to decrease to be in line with its long-run trend. Other explanatory variables are previous changes in both the bank and policy rates (

, the speed of adjustment (or error-correction coefficient), is expected to be negative: if the banking rate is higher than it should be (as predicted by the long-run relationship), it is likely to decrease to be in line with its long-run trend. Other explanatory variables are previous changes in both the bank and policy rates (![]() , the time trend, and

, the time trend, and ![]() , the short-run effects of the policy rate).

, the short-run effects of the policy rate). ![]() is a dummy variable equal to 1 when the policy rate is below 0, making

is a dummy variable equal to 1 when the policy rate is below 0, making ![]() the interaction variable between changes in the policy rate when the rate is negative. In other words,

the interaction variable between changes in the policy rate when the rate is negative. In other words, ![]() (resp.

(resp. ![]() ) captures the effect of a change in t (resp. t-1) of the monetary policy rate on changes in the bank rate and

) captures the effect of a change in t (resp. t-1) of the monetary policy rate on changes in the bank rate and ![]() the additional effect when the rate is negative. If

the additional effect when the rate is negative. If ![]() is not null and statistically significant, this would mean that the adjustment of banking rates with regard to the policy rate changes when rates are negative.

is not null and statistically significant, this would mean that the adjustment of banking rates with regard to the policy rate changes when rates are negative.

In other words, the objectives of this second analysis are, first, to assess how a change in the bank rate can be explained by a change in the policy rate in the previous period (short-run effect of the policy rates), and second, to see whether negative policy rates change the way in which the policy rate impacts bank rates (is the pass-through of policy rates to banking rates different when rates are negative, because banks avoid setting extremely low or negative rates for corporations and households?).

While the coefficients of the short-term changes in the policy rate confirm that the pass-through is stronger for banks’ assets (loans) than for their liabilities (deposits), as well as for corporate rates, the effect of the interaction variable is not statistically significant. This suggests that there is no change in the relationship between the policy rate and bank rates when the policy rate is negative. In other words, nothing indicates the presence of non-linearity of the effect below the threshold of zero. We tested other thresholds by steps of 10 bps below 0% (-0.1%, -0.2%, etc. down to -0.5%) and found similar results.

Our results imply that while rate cuts compress banks’ interest margins, we failed to find any evidence of a non-linearity of this effect below 0%. Monetary easing appears to have a negative impact on banks’ net interest margins at least directly, because indirectly an improvement in the economy due to the easing could counterbalance this effect in the medium to long run. For instance, one important channel leading to improvement at the macro level is that the banks’ loss of interest margins represents a gain for households and corporations through cheaper borrowing, while the rate on deposits does not fall as much. But rate cuts in negative territory do not seem to amplify this negative impact on banks’ margins in a significant way.

The fact that rates on households’ deposits are still above 0% is generally interpreted as a non-linearity: banks are not passing negative rates through to households’ deposits because they are afraid cash will start to be withdrawn. But it is also possible that this rate is still above 0% because of its usual stickiness. For instance, some banks have started passing through negative rates to their corporate deposit rates (which are generally more sensitive to rate cuts), despite the risk of cash hoarding by non-financial corporations (NFC), similarly to households: the average euro-area rate on NFCs’ overnight deposits is still positive, but the averages in Germany and the Netherlands are negative.

Despite negative rates, corporations and households are not converting their deposits into cash yet, probably because the negative rate applied to deposits is still lower than the cost of storing cash and/or because of the convenience of bank deposits and electronic payments (especially with the recent increase in online shopping).

Nevertheless, our results also mean that the effect of rate cuts (whether below or above the zero lower bound) on banks will depend on their financial structures, and on the composition of their assets and liabilities (which differs across banks and across countries): if a bank is heavily reliant on households’ deposits and if lending rates to households and corporations decrease more steeply than the rates applied to deposits, then its net interest income will be particularly reduced. The literature generally shows that, on average in the euro area, banks’ overall profitability has not been significantly affected by the introduction of negative rates, in part because increased asset values and stronger economic activity have offset the negative effects. But the literature also suggests that banks with higher shares of households’ deposits have either seen their profitability more affected by the fall in rates, or that they have not passed the rate cuts to their loans to try to compensate.

There are two important caveats to our analysis. First, the evidence has been gathered with negative rates relatively close to 0%. This means that a strong non-linearity could still arise at lower rates. Second, the impact on banks could also vary over time. Effects of prolonged negative rates could be different: at the beginning, the effect might be positive as the one-off mark-to-market revaluation dominates, but, if negative rates are prolonged, maturing assets might be gradually replaced by low-yielding loans, which could lead to a persistent decline in interest margins. In addition, the reduction of net interest income, compensated for at the beginning by higher volumes and increased fees, might not last – or banks will have to adjust their business models in order to rely more on fees than on interest margins.

Recommended citation:

Claeys, G. and L. Guetta-Jeanrenaud (2021) ‘How have the European Central Bank’s negative rates been passed on?’ Bruegel Blog, 7 July

Republishing and referencing

Bruegel considers itself a public good and takes no institutional standpoint. Anyone is free to republish and/or quote this post without prior consent. Please provide a full reference, clearly stating Bruegel and the relevant author as the source, and include a prominent hyperlink to the original post.