Blog Post

Blogs review: The safe asset shortage

What’s at stake: Safe debts – or what is often called information insensitive assets, as they do not suffer from the types of financial frictions that are characteristic to other financial assets – play a major role in facilitating transactions for institutional investors. And, as we have learned in the recent years, they also play a major role in triggering financial crises when they loose their safety status and turn into information sensitive assets. As central bankers start backpedalling on their commitments to increase the supply of safe assets and start worrying about the negative effects of the “search for yield”, there has been a renewed discussion in the blogosphere about the role of safe assets and whether they remain in short supply.

What’s at stake: Safe debts – or what is often called information insensitive assets, as they do not suffer from the types of financial frictions that are characteristic to other financial assets – play a major role in facilitating transactions for institutional investors. And, as we have learned in the recent years, they also play a major role in triggering financial crises when they loose their safety status and turn into information sensitive assets. As central bankers start backpedalling on their commitments to increase the supply of safe assets and start worrying about the negative effects of the “search for yield”, there has been a renewed discussion in the blogosphere about the role of safe assets and whether they remain in short supply.

The role and evolution of safe assets

Gary Gorton, Stefan Lewellen, Andrew Metrick write that to the extent that debt is information-insensitive, it can be used efficiently as collateral in financial transactions, a role in finance that is analogous to the role of money in commerce. It is in this respect that information-insensitive or “safe” debt is socially valuable. In a chapter of the Global Financial Stability Report, the IMF writes that safe assets have four main functions: they are a reliable store of value, they provide safe collaterals, they serve as benchmarks to measure the relative risks of other assets, and have become a key ingredient to the prudency framework for banks.

Timothy Taylor send us to Gary Gorton, Stefan Lewellen, Andrew Metrick who have written a rare academic papers with a basic empirical finding that shakes up your mental landscape. They note that over the past sixty years, the total amount of assets in the United States economy has exploded, growing from approximately four times GDP in 1952 to more than ten times GDP at the end of 2010. Yet within this rapid increase in total assets lies a remarkable fact: the percentage of all assets that can be considered “safe” has remained very stable over time. Specifically, the percentage of all assets represented by the sum of U.S. government debt and by the safe component of private financial debt, which we call the “safe-asset share”, has remained close to 33 percent in every year since 1952.

The demand for safe assets and financial crises

Gary Gorton (HT Timothy Taylor) thinks that the way we think of crises in mainstream macroeconomic models – as being the result of a shock that then gets amplified – is misleading. We see a few really big events in history: the recent crisis, the Great Depression, the panics of the 19th century. Those are more than a shock being amplified. It’s a regime switch — a dramatic change in the way the financial system is operating. This notion of a kind of regime switch, which happens when you go from debt that is information-insensitive to information-sensitive, is conceptually different than an amplification mechanism.

Carola Binder helps us walk through the new paper by Gary Gorton and Guillermo Ordoñez called "The Supply and Demand for Safe Assets." In the model, there are normal times and crisis times. In normal times, the average land quality (a modeling simplification that basically encompasses all types of private collateral) is high enough that lenders are better off NOT paying the fixed cost to check the quality of the land (they’re information insensitive). The inefficiency from the financial friction is, therefore, avoided. However, there can be shocks to the average quality of land. Land quality may get low enough that lenders need to check the land quality before they accept it as collateral, resulting in economic inefficiency and a financial crisis. This is where Treasuries come in. Government bonds can also be used as collateral, and they don’t suffer losses in value like land does.

David Beckworth explains that safe assets facilitate transactions for institutional investors and therefore effectively acts as their money. During the crisis, many of these transaction assets disappeared just as the demand for them was picking up. Since these institutional money assets often backstop retail financial intermediation, the sudden shortage of them also meant a shortage of retail money assets.

The excess demand for safe assets and the excess supply of goods

Brad DeLong sends us to an oped he wrote in 2010. In 1829, John Stuart Mill made the key intellectual leap to connect these two things. Mill saw that excess demand for some particular set of assets in financial markets was mirrored by excess supply of goods and services in product markets, which in turn generated excess supply of workers in labor markets. If you relieved the excess demand for financial assets, you also cured the shortfall of aggregate demand [for a recent formulation of these arguments, see Ricardo Caballero and Emmanuel Farhi].

· When the excess demand is for liquid assets used as means of payment – for “money” – the natural response is to have the central bank buy government bonds for cash.

· When the excess demand is for longer-term assets – bonds to serve as vehicles for savings that move purchasing power from the present into the future – the natural response is to induce businesses to borrow more and build more capacity, and encourage the government to borrow and spend.

· When excess demand is for high-quality assets – places where you can park your wealth and be assured that it will still be there when you come back – the natural response is to have credit-worthy governments guarantee some private assets and buy up others.

One way to understand European austerity is to say that yes having governments spend more money and continue to run large deficits will increase the supply of bonds and will thus relieve the shortage of longer-term assets. But if a government’s debt emissions exceed its debt capacity, all of that government’s debt will become risky and will thus create a shortage of high-quality assets.

Excess demand: why isn’t the price of these assets just adjusting?

JP Koning (HT David Beckworth) asks a great question: Why do we *need* more safe assets? Why don’t we just let the existing ones rise in value, thereby providing safety? The great thing about T-bonds is that unlike goods that could be purchased as a safety vehicle, we don’t need to fabricate more of them to meet our demands for safety. We just need a higher real value on the stock of existing T-bonds. This can be entirely met by shifts in prices.

David Beckworth writes that the problem is that safe assets, treasury securities in particular, cannot make this adjustment when they are up against the zero lower bound (ZLB). Given the large shortfall of safe assets, interest rates need to go below 0% for treasury prices to rise enough to satiate the excess demand for them. Investors, however, can earn 0% holding money at the ZLB.

David Beckworth writes that the short answer to Koning’s question is that the ZLB has segmented the transaction asset market and this is preventing the safe asset market from clearing. The heightened economic uncertainty and the ZLB means the demand for these transaction assets (i.e. money and treasuries) becomes almost insatiable. Investors, therefore, shy away from other higher yielding. Treasuries and money become increasingly close substitutes as they approach the ZLB, while the overall transaction asset market becomes increasingly segmented from other asset markets. Market segmentation is a controversial idea. Many observers don’t accept it. But it seems like a compelling story for the transaction asset market at the ZLB. Empirically, it provides an easy explanation for why BAA-AAA corporate yield spread, junk bond spread, and other non-transaction asset spreads are getting closer to historical norms, while the BAA yields-10 treasury yield spread and the S&P500 earnings yield-20 year treasury yield spread remain inordinately high.

Paul Krugman considers that the search for safety is a distinctly secondary factor in explaining the low interest rates that we observe. Consider the example of Japan. For the last 15 years, long-term rates have been stuck at an extremely low level. So what explains this? Safe assets didn’t seem to be in short supply in, say, 2005, when investors believed in the virtues of toxic waste. But the key point about Japan is that anyone who bought and held those bonds made money, because short rates were close to zero throughout. I guess my point is that the “safe asset” meme seems to imply that there’s some kind of market aberration in the high prices (and low yields) of bonds, that investors are willing to lose money because they’re frightened. But most of what we’re seeing just reflects a perceived lack of good investment opportunities.

Excess demand: why isn’t there more supply?

Why then, is it hard to create safety? Ricardo Caballero writes in VoxEU that even credible private actors which transform financial micro-, localized risks are not equipped to create safe assets which cover macro-, aggregate risks. Streams of revenues can be securitized and tranched to create a ‘safe asset’, but when all the underlying loans default, only a macroeconomic actor can step in.

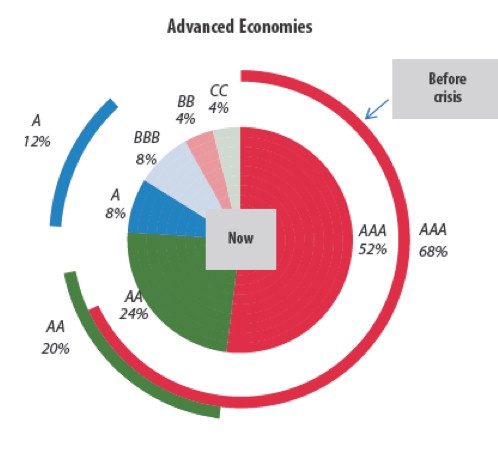

Should we worry about public deficits becoming too small? Matthew C. Klein writes that by providing collateral, government bonds are complement, not substitute, of private debt. Such concerns had already surfaced under the Clinton administration: Carolina Binder refers to a report written in the late 1990s, when economists started to fear that public surpluses would starve the market of safe public instruments and lead to instability in the markets. But of course, governments are themselves limited by a sustainability constraint on their debt. FT Alphaville even terms ‘most important chart of the world’ this picture of government bonds disappearing from the ‘safe’ category. Another way to picture it comes from the IMF:

Source: IMF (p. 107)

International causes and consequences

This perspective also brings many insights in the working of international economics. As described by Ricardo Caballero, the lack of saving vehicles for savers in emerging market countries triggered a demand for short-term government or other government guaranteed bonds, and then other types of corporate bonds. By 2001, as the demand for safe assets began to rise above what the US corporate sector and safe-mortgage-borrowers naturally could provide, financial institutions began to search for mechanisms to generate triple-A assets from previously untapped and riskier sources. As shown by Hyun Song Shin, international banks, and especially European, also tapped this wholesale market for liquidity. According to him, the global banking glut, rather than saving glut, is to blame for the build-up leading to the financial crisis.

In a recent paper, Olivier Gourinchas and Olivier Jeanne argue that eventually a safe assets had to be backstopped by a monetary authority that the euro area lacks. They thus conclude that in the aftermath of the crisis, the dollar was reinforced as currency of denomination for safe assets (and global banking).

Republishing and referencing

Bruegel considers itself a public good and takes no institutional standpoint. Anyone is free to republish and/or quote this post without prior consent. Please provide a full reference, clearly stating Bruegel and the relevant author as the source, and include a prominent hyperlink to the original post.