Blog Post

Blogs review: Asset prices and monetary policy redux

What’s at stake: Federal Reserve Governor Jeremy Stein gave serious consideration to the idea that monetary policy has a role to play in managing financial stability (read asset prices) in a speech titled “Overheating in Credit Markets: Origins, Measurement, and Policy Responses” given last week at a conference hosted by the St. Louis Fed. Governor Stein provided evidence that risk was building in certain segments of financial markets and discussed policy tools that go beyond countercyclical macroprudential regulation or the simple use of the Federal Funds rate to address these risks.

What’s at stake: Federal Reserve Governor Jeremy Stein gave serious consideration to the idea that monetary policy has a role to play in managing financial stability (read asset prices) in a speech titled “Overheating in Credit Markets: Origins, Measurement, and Policy Responses” given last week at a conference hosted by the St. Louis Fed. Governor Stein provided evidence that risk was building in certain segments of financial markets and discussed policy tools that go beyond countercyclical macroprudential regulation or the simple use of the Federal Funds rate to address these risks.

Questioning the Greenspan-Bernanke orthodoxy

Free Exchange writes that before the crisis, monetary policymakers generally agreed that they should not concern themselves with financial stability until after something bad had already happened. Prevention was the job of the regulators, they said. Ben Bernanke and Mark Gertler made the most comprehensive case for this hands-off approach in 1999. A few dissented, such as the Bank for International Settlements’ dynamic duo of Claudio Borio and William White, as well as Raghuram Rajan of the University of Chicago. But the establishment mostly ignored them until the crisis.

Neil Irwin writes at the Wonkblog that it’s good to see leaders of the Fed grappling—in their cerebral, cautious way, at least—with an issue that has seemed apparent to many in financial markets for years: That low interest rate policies and unconventional easing programs such as Fed bond purchases can have hard-to-predict results throughout the financial system beyond those that traditional models of how monetary policy affects the economy would predict.

The incentives of financial intermediaries and the search for yield

Governor Jeremy Stein argued that a change in the economic environment that alters the risk-taking incentives of agents making credit decisions could lead to overheating. For example, a prolonged period of low interest rates, of the sort we are experiencing today, can create incentives for agents to take on greater duration or credit risks, or to employ additional financial leverage, in an effort to “reach for yield.” If the underlying economic environment creates a strong incentive for financial institutions to, say, take on more credit risk in a reach for yield, it is unlikely that regulatory tools can completely contain this behavior.

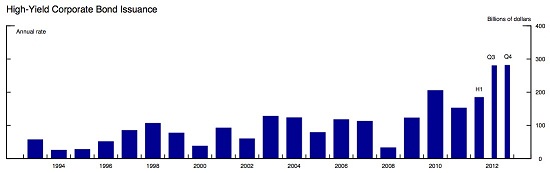

Gavyn Davies writes that the speech argues that the credit markets have recently been “reaching for yield”, much as they did prior to the financial crash. Although not yet as dangerous as in the period from 2004-2007, this behavior is shown by the rapid expansion of the junk bond market (see Figure), flows into high-yield mutual funds and real estate investment trusts and the duration of bond portfolios held by banks. Governor Jeremy Stein argues that overheating in the junk bond market although not a major systemic concern in and of itself might indicate that similar overheating forces are at play in other parts of credit markets, out of our range of vision.

Source: Jeremy Stein

Policy implications: principles and historical precedents

Governor Jeremy Stein argues that as we move forward, and assuming that the trends in asset-liability mismatch identified continue, it will be important to keep an open mind and avoid adhering to the decoupling philosophy – that monetary policy should restrict its attention to the dual mandate goals of price stability and maximum employment, while the full battery of supervisory and regulatory tools should be used to safeguard financial stability – too rigidly. While monetary policy may not be quite the right tool for the job, it has one important advantage relative to supervision and regulation–namely that it gets in all of the cracks. The one thing that a commercial bank, a broker-dealer, an offshore hedge fund, and a special purpose vehicle have in common is that they all face the same set of market interest rates.

Scott Sumner wonders how much Mr. Stein knows about Fed policy during the 1920s. The paper does not mention that 1929 was the last time the Fed tried to implement his proposed policy. During the 1920s NY Fed President Benjamin Strong was under a lot of pressure to “do something” about the stock market boom. He resisted, arguing the Fed should focus on stabilizing prices and output. He died in August 1928, and the new leaders of the Fed finally had their chance. They raised interest rates in late 1928, and then in early 1929, and then in mid-1929. By the late summer of 1929 short-term rates were at 6%. Recall that this was a very high real rate, as there was deflation during the 1927-29 business cycle expansion, despite the fact that the economy was booming. Finally money got so tight that the economy tipped into depression. And it was (expectations of) the depression that caused the stock market crash, not the high interest rates.

Berkeley PhD student Carola Binder writes in her new blog Quantitative Ease that the Fed also regarded bubbles as the most likely negative consequence of its efforts to reduce unemployment by stimulating growth in 1953-54. In 1955, as the economy was recovering, the minutes from the Federal Open Market Committee refer multiple times to concerns about "speculative developments" or "speculative excesses." The March 2 minutes note: “The critical problem for credit and monetary policy in the United States was […] how to thread its way along the narrow ledge that encourages sound economic growth and high employment and, at the same time, limits speculative developments and discourages financial over commitments by businesses and consumers.”

Ryan Avent writes that we should not let the lessons of the last disaster obscure the lessons of the ones that came before.

In a 2010 paper for the BIS titled "the changing role of central banks", Charles Goodhart argues that the question is not whether a Central Bank that sets interest rates should also manage financial stability but whether a Central Bank that manages both liquidity and financial stability should also be given the task of setting interest rates. Unlike the essential role of liquidity management, setting official interest rates is not essential for a Central Bank. In history many central banks did not set interest rates and this task was left to the government or to an external committee.

Charles Goodhart argues that in the 19th century, the BoE had an intellectual framework that dealt with the trade-off between price stability and financial stability. It was the real bills doctrine. So long as discounts and lending were strongly directed to ‘real bills’, both price stability and financial stability were supposed to be jointly and simultaneously assured. The "real bills " led to mistakes and policy failures during the interwar but "ever since this Victorian era we have lacked such a unifying theory. So now we wonder whether the single interest rate instrument can, or should, be made to bear double duty, to ‘lean into the wind’ of asset price and credit fluctuations as well as stabilizing inflation, and its expectations".

Policy proposal: changing the composition of asset holding even after the ZLB

Governor Jeremy Stein has a particular proposal in response to concerns about numbers of instruments. We have seen in recent years that the monetary policy toolkit consists of more than just a single instrument. We can do more than adjust the federal funds rate. By changing the composition of our asset holdings, as in our recently completed maturity extension program (MEP), we can influence not just the expected path of short rates, but also term premiums and the shape of the yield curve. Once we move away from the zero lower bound, this second instrument might continue to be helpful, not simply in providing accommodation, but also as a complement to other efforts on the financial stability front.

John Cochrane argues that once the central bank does something else than setting interest rates and conducing open market operations, the risk to interfere and distort markets is high. Cochrane argues that an agency that allocates credit to specific markets and institutions, or buys assets that expose taxpayers to risks, cannot stay independent of elected, and accountable, officials.

Also of note is a 2012 paper Jeremy Stein where the author models the market imperfection that leads to the need of central bank’s intervention to maintain financial stability. When banks issue cheaper short-term debt, they capture the social benefits (liquidity for households) but do not fully internalize the costs (fire sales in case of adverse shocks) of such actions. The author favors a “cap-and-trade” system in which banks are granted tradable permits, each of which allows them to do some amount of money creation.

Republishing and referencing

Bruegel considers itself a public good and takes no institutional standpoint. Anyone is free to republish and/or quote this post without prior consent. Please provide a full reference, clearly stating Bruegel and the relevant author as the source, and include a prominent hyperlink to the original post.