Blog Post

Blogs review: The Fiscal Cliff

What’s at stake: In an update to its budget and economic outlook, the Congressional Budget Office (CBO) reminded of the approaching “fiscal cliff” – a popular wonk-speak used to describe the significant automatic cuts in federal spending and tax increases scheduled to take place at year end under current laws. CBO estimates that the fiscal drag would be in the order of 4% and would cause a double-dip recession. But even before the issue of the actual economic drag such an impulse could create lies the question of how potential political scenarios could shape policy outcomes, especially ahead of the Presidential election.

What’s at stake: In an update to its budget and economic outlook, the Congressional Budget Office (CBO) reminded of the approaching “fiscal cliff” – a popular wonk-speak used to describe the significant automatic cuts in federal spending and tax increases scheduled to take place at year end under current laws. CBO estimates that the fiscal drag would be in the order of 4% and would cause a double-dip recession. But even before the issue of the actual economic drag such an impulse could create lies the question of how potential political scenarios could shape policy outcomes, especially ahead of the Presidential election.

How big, where and when

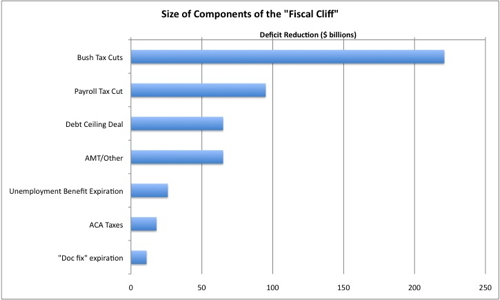

The CBO report estimates that if current laws generally remain in place, the deficit will shrink to an estimated $641 billion in fiscal year 2013 (or 4.0 percent of GDP). The diagram below illustrates the main components of the cliff: the expirations of the Bush administration income tax cuts and of the payroll tax cut that was part of Obama’s 2011 jobs plan, vast cuts (sequestration) of discretionary spending as consequence of the debt ceiling deal, no inflation indexation of the Alternative Minimum Tax cut-off (a tax increase for people being pushed into the range of the AMT) and the expiration of extended unemployment benefits.

Source: The Wonkblog

Dylan Matthews gives the timing of these measures. The payroll tax break expires this December, and the Bush tax cuts expire Jan. 1, meaning that new, higher rates will take effect the following year. Since payroll taxes are deducted from wages every week, the effect there will be immediate, whereas the income tax rate increases only affect income starting in 2013. If employers adjust withholding, the effects could come sooner, but if there are logistical hurdles to that, the economic dent could be delayed. The sequestration cuts will take effect starting in January too, meaning their impact, like the payroll tax cut’s expiration, will be more immediate. The cuts are evenly split, with $27 billion each in 2013 for defense and non-defense spending, plus $12 billion in cuts to Medicare.

Economic impact of the fiscal cliff: multipliers, incentives, and budget balancers

In his statement in front of the Senate Committee on the Budget, Douglas W. Elmendorf – director of the CBO – argued that such fiscal tightening will lead to a 3.9 percent reduction in the growth rate of GDP next year — enough to make economic conditions in 2013 recessionary, with real GDP declining by 0.5 percent between the fourth quarter of 2012 and the fourth quarter of 2013 and the unemployment rate rising to about 9 percent in the second half of calendar year 2013. Greg Ip writes that actually, the recession would probably be worse. Given the inability of the Federal Reserve to meaningfully compensate, such a fiscal hit is liable to set off a self-reinforcing spiral of declining consumption and income, falling inflation and rising real interest rates.

Casey Mulligan argues that the CBO analysis for 2013 is based on the Keynesian proposition that anything that shrinks the federal budget deficit shrinks the economy, and the more the deficit is reduced the more the economy is reduced. In many circumstances, the Keynesian proposition reaches the wrong conclusions about economic activity, because it ignores incentives of all kinds, as pointed out by John Cochrane in a recent post. Perhaps the incentive-reducing provisions of the fiscal cliff outweigh its incentive-enhancing provisions, in which case the Congressional Budget Office has arrived at approximately the right answer for the wrong reasons. But even in that lucky case, the C.B.O.’s quantitative estimates of the fiscal cliff’s economic effects are not reliable until they fully incorporate economic incentives.

Edward Lazear writes that Keynesians see tax increases and spending decreases as a lose-lose for the economy, while supply-siders – such as Mulligan and Cochrane – see the coming fiscal changes as a mixed bag. Another perspective comes from the oft-ignored school of thought of budget balancers, who see the coming package as a win-win for the long-term outlook. They argue that a government that takes on unsustainable debts in the short-term will mortgage its long-term prospects, and therefore elimination of budget deficits should be prioritized.

Predictable risks, hidden threats and likely scenarios

Greg Ip writes that the focus on the fiscal cliff is a bit of a distraction. The fact that it is such a large and predictable risk is why Congress is highly unlikely to let it happen (except perhaps for a few weeks, between December 31st and the inauguration of a new president later in January). Here’s the real threat. Even if the Bush tax cuts are extended and the sequester delayed, a huge amount of fiscal drag remains in place. ISI Group projects $220 billion of fiscal tightening in 2013, or 1.4% of GDP. JPMorgan, noting that many Recovery Act programmes are rolling off at the same time, puts the hit at a slightly higher $266 billion, or 1.7% of GDP. The IMF reckons fiscal policy will tighten more in America next year than in Spain, Italy or Portugal.

Dylan Matthews argues that as a Grand Bargain is improbable in present US politics, what is most likely is this: Letting the Bush and the payroll tax cuts expire (as the Democrats don’t want to extend the former and no-one wants to indefinitely extend the latter), but averting the other cliff elements (spending cuts, unemployment benefit expiration, reduced Medicare rates) from kicking in. This will still reduce growth, but a lot less than the full fiscal cliff would. Another conjuncture smoothing scenatio is suggested by Ed Nolan: the elements of a compromise must be revenue-raising tax reform based primarily on base-broadening, expenditure discipline on non-growth-enhancing items as well as Social Security and Medicare reform. Dean Baker, on the other hand, thinks that as the cliff is initially not that steep, the Democrats can take the time to first let the tax cuts expire, and then propose to restore tax cuts but only for the bottom 98% of the population – a proposal that the Republicans could hardly afford to resist.

Peter Orszag writes that with the US being characterised by strong polarisation of the political factions, the best thing to do is to expand the degree of policy “automaticity” (such as linking stimulus to objective criteria). The automatic expiration of tax cuts in the cliff is a case in point, as it will create more scope for deals than previously existed. The proposed scenario involves the Democratic administration first allowing the tax cuts to expire, then propose a progressive tax cut that the Republicans will find hard not to support, such as a large payroll tax holiday together with an increase in the standard deduction. The spending sequester could be undone In return for some entitlement changes in Social Security, Medicare and Medicaid.

Alec Phillips of Goldman Sachs thinks that fiscal restraint will be greatest in 2013 if the US remains at the status quo of divided government. The risk that these policies could temporarily lapse in Q1 2013 is greatest under a scenario where control of the House, Senate and/or White House changes hands, leading to unexpected fiscal restraint and policy uncertainty. The presidential and congressional elections on November 6 will play an important role in determining which policies will be phased in or out on schedule and which will be postponed. While the congressional election outcome does not take effect until January 3, 2013 and the presidential election outcome does not take effect until January 20, 2013 once the results become known in early November, they are apt to immediately influence deliberations on fiscal matters. By contrast, a status quo outcome that preserves a divided government would imply a lower likelihood of a temporary lapse, but could lead to somewhat greater fiscal restraint in 2013 because of the difficulty in delaying the sequester, of a greater potential for a tax increase; and of lower likelihood of additional fiscal stimulus. Alec Phillips also notes that the statutory debt limit is also likely to require another increase around the end of the year, which will necessitate legislation. If the binding deadline to enact debt limit legislation falls before the end of 2012, this could very easily become a vehicle to address–even if only on a temporary basis– some of the issues noted above.

Republishing and referencing

Bruegel considers itself a public good and takes no institutional standpoint. Anyone is free to republish and/or quote this post without prior consent. Please provide a full reference, clearly stating Bruegel and the relevant author as the source, and include a prominent hyperlink to the original post.