Blog Post

Internationalisation of Asian Currencies and the International Monetary System

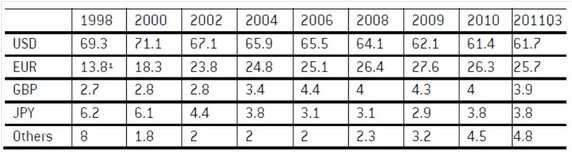

The US dollar still accounts for more than 60 percent of foreign exchange reserves held worldwide, but history tells us that large macroeconomic changes are usually followed by important changes in the monetary system. Yet these changes are not mechanic and rarely abrupt. Eichengreen and Flandreau (2011) recently highlighted how the pound sterling was overtaken […]

The US dollar still accounts for more than 60 percent of foreign exchange reserves held worldwide, but history tells us that large macroeconomic changes are usually followed by important changes in the monetary system. Yet these changes are not mechanic and rarely abrupt. Eichengreen and Flandreau (2011) recently highlighted how the pound sterling was overtaken by the US dollar as the world leading currency in the interwar period and was eventually crowned as the central currency of the international monetary system after Bretton Woods. The collapse of the Bretton Woods system opened the possibility of a challenger to the dollar but the contenders have been moderately successful so far. The internationalisation of the Japanese yen in the early 1980s effectively halted after the Japanese banking crisis of the early 1990s and receded after the launch of the euro which until recently was largely seen as the most serious challenger to the dollar.

Table 1 International currencies in foreign exchange reserves (percent)

Note: 1) Based on Deutsche mark.

Sources: IMF, Currency Composition of Official Foreign Exchange Reserves 2011 till 2010 and BIS Quarterly Review, December 2011 for 2011.

Japan’s large trade surplus with the US throughout the late 1970s and early 1980s motivated the internationalisation of the Japanese yen in Asia. It began with the liberalisation of its financial market and the opening up of its banking system to foreign participation but progresses were modest, the monetary boom of the 1980s partly provoked by the G7 interventions to weaken the yen eventually led to an asset bubble which collapsed in the early 1990s thereby undermining profoundly the internationalisation strategy of the yen. With a bankrupt banking system which sank further following the Asian crisis of 1997, Japan couldn’t possibly use its feeble banking giants to turn itself into the world’s banker and thereby establish the yen as a leading reserve currency. The advent of the euro slowly contributed to sideline the yen further by shifting financial might on the European continent.

Table 2 Foreign exchange transactions and international bonds

Proportion of Daily Foreign Exchange Transaction Amount (percent) Issuance of International Bonds (in billions of US dollars)

Source: BIS, Quarterly Review, March 2011, Triennial Central Bank Survey.

BIS Quarterly Review, December 2011

Yet the experience of the euro is too short to be fully conclusive and the ongoing crisis an important challenge. Even before that, Europeans were divided over the importance of the international standing of their currency and the ECB has showed during the crisis that it was only moderately interested in assuming the role of an international lender of last resort which ought to be a defining feature of true leading reserve currency. In addition, there are idiosyncratic European challenges: the euro area’s financial centre remains in a non euro area country and the share of the euro in international reserves as well as in international issuance has receded. All in all, the consensual trajectory towards a bipolar international monetary system therefore seems to be somewhat put to test.

Indeed, outside of growing uncertainty weighing on the two leading currency areas, two important events seem to be shaping the international monetary system. One is the growing fragmentation of the world economy order with diminishing influence of the center and growing influence of the periphery. The other is the growing contestation of the current monetary order regarded as both inefficient and unjust by the emerging world and by China in particular.

Indeed since 2009, China has expressed the clear willingness to reduce its dependency on the dollar and expand the role of its own currency in international transactions. Recently, China has launched important an pilot scheme to broaden the use of the RMB in trade settlements transactions followed with a large number of bilateral currency swap arrangements aiming at distributing RMB internationally as and when necessary. In addition, the creation of the RMB offshore market in Hong Kong has allowed circumventing a number of capital account restrictions and bypassing financial regulations that govern the domestic RMB market which would have both limited the use of the RMB in international transactions. Yet, it is unclear what is the ultimate Chinese strategy with respect to its currency and the IMS. Will China seek to establish the RMB as a regional anchor as a stepping-stone to its global ambitions? While Japan seems to have given up its international ambitions for the yen by signing up to a bilateral agreement with China to promote the use of the RMB in regional transactions, other Asian countries might not be prepared to stick to their orbit around the RMB so soon. India is a clear example, Korea also seems tempted by the internationalisation potential of its own currency and Australia is also enjoying a wave of interest by international reserve managers that might be difficult to give up. There will therefore be a degree of domestic competition before a regional anchor emerges. This has important ramification for international financial cooperation in the region, in particular for the creation of a stable safety net mechanism and an effective multilateral surveillance framework. In this respect, the ongoing reforms of the Chiang Mai Initiative are encouraging on the safety nets front and incomplete on the surveillance side.

It is also unclear whether China seeks a hegemonic role in the monetary system to overtake the United States or whether it simply wants a more balanced distribution of the reserve currency dividends and a fairer say in global economic governance. In brief, is China seeking to replace the current global monetary dominance by another or is it helping to move towards a more multilateral or multipolar international monetary system. Chinese authorities themselves might not even precisely know the precise answer to this question and it is, in fact, likely to be largely path dependent. This is precisely why the current discussions surrounding the legitimacy of the G20 and the governance of the IMF are key. The faster Asia comes to play a role at the IMF that is commensurate with its importance in the world economy, the higher the chances that it will engage in currency reform in a way that is most compatible with the stability of the international monetary system and the efficiency of the world economy. International economic cooperation is never a given, it is always a struggle.

Republishing and referencing

Bruegel considers itself a public good and takes no institutional standpoint. Anyone is free to republish and/or quote this post without prior consent. Please provide a full reference, clearly stating Bruegel and the relevant author as the source, and include a prominent hyperlink to the original post.